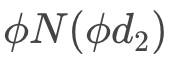

These could be premium adjusted deltas. Essentially the delta would have been adjusted by the amount of the option premium in foreign currency. Re-comment, here is the formula for the premium adjusted ATMF delta (note \phi=1 for call and -1 for put):