The EBA performs the HDP (high default portfolio) and LDP (low default portfolio) benchmarking exercises, which would be relevant. You can find it on their website. Here are a couple of examples:

Re-comment, I think it is clearer in the summary table in the latest survey which includes both HDP and LDP (https://eba.europa.eu/documents/10180/2087449/EBA+Report+results+from+the+2018+Credit+Risk+Benchmarking+Report.pdf):

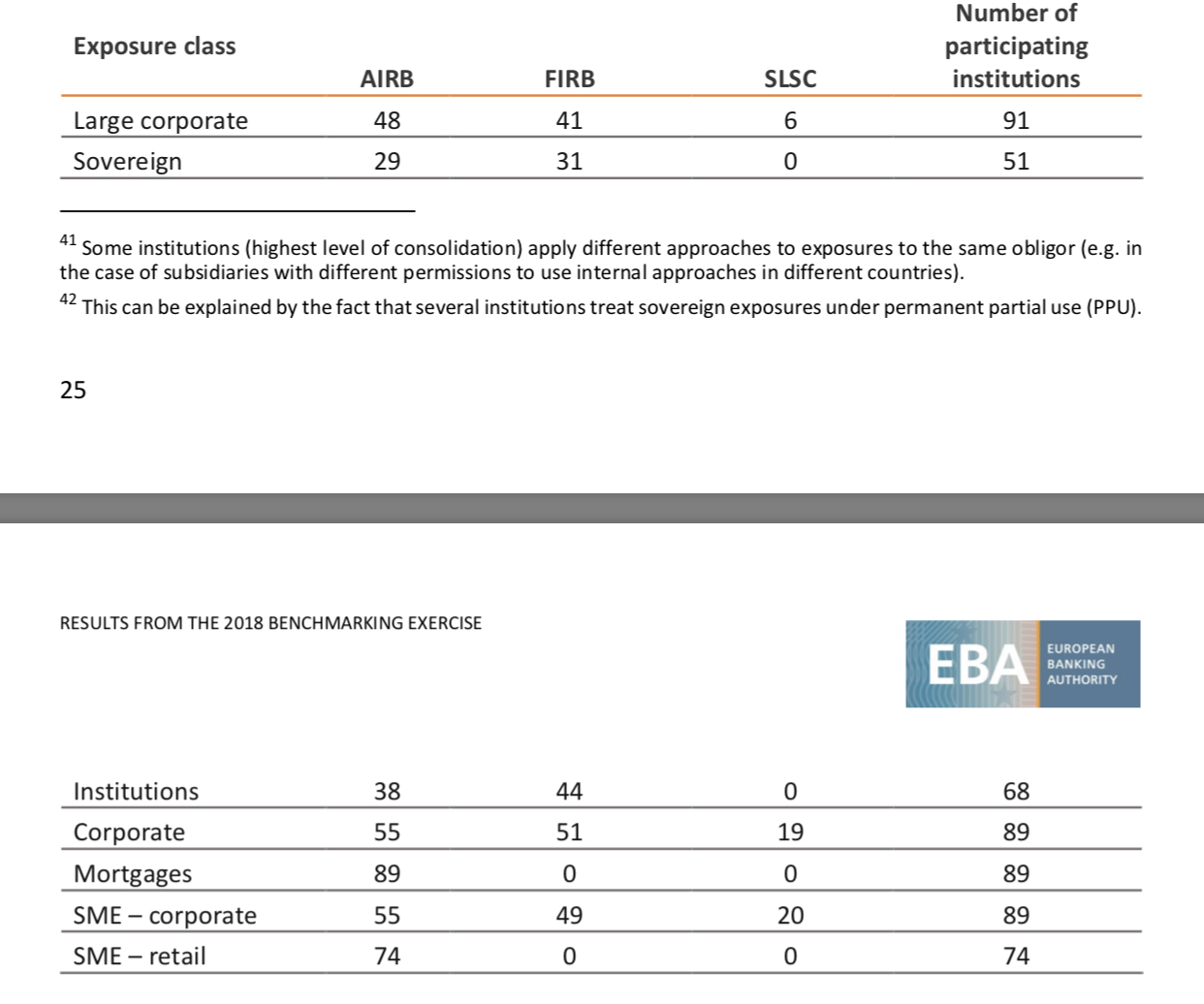

The intro says 117 institutions have permission for credit models, of which 114 submitted the data, so I think the sample is representative and they have even explained why the 3 did not. The reason the number of institutions differ by asset class is because not all of them would have exposure to all classes/samples. And the rows don’t add up to the total institutions could be because of footnote 41, same institution using different approaches in different countries. The report also claims the results are stable compared to previous survey, implying quality is ok I suppose.