Main question: Do we need to restrict the vol-of-vol parameter in SABR further than $\text{vol-of-vol}>0$ and how do we determine the interval of vol-vol which the model is arbitragefree?

Background

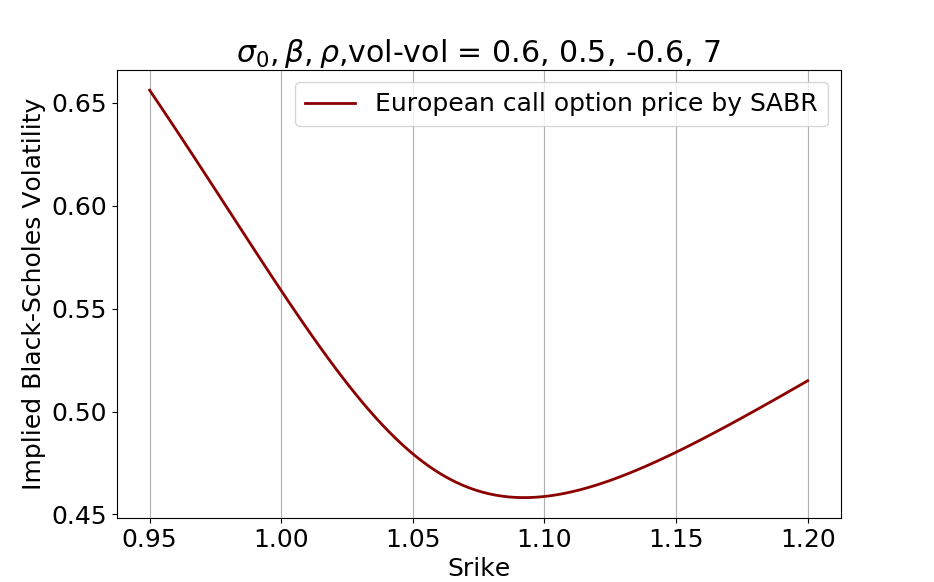

Please consider a SABR model and an asset with time 0 price at $S_0=1$. Say we want the 1 year call option prices ($T= 1$) and the rate is zero $r = 0$. With the SABR parameters shown in the figure we get this:

The vol-vol parameter is extremely high at 7 (unlikely process, I know.) But this pricing will totally lead to Arbitrage because call with strike 1.15 is more expensive than call w. strike 110.

I have now gone through countless of papers on SABR and no-one mentions this problem. That at some point higher vol-vol might lead to arbitrage?

Info

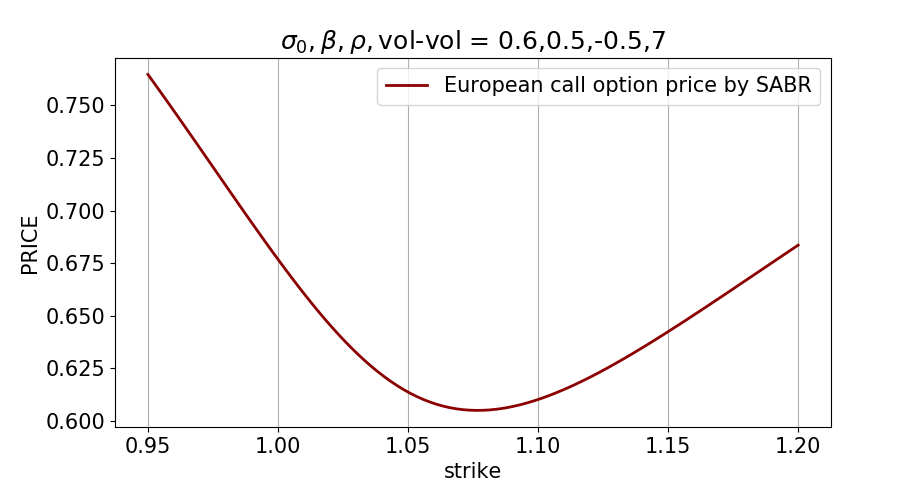

The call option prices are computed such that

- I have used Hagan formula to compute the implied vol

- I have put the implied vol into the Black Scholes pricing formula as the volatility

For instance: $IV = HAGAN(k=1.15; \sigma_0,\beta,\rho,vol-vol) = 1.93$

$$BS_{call} = (\sigma = IV ; ....) = 0.6425$$