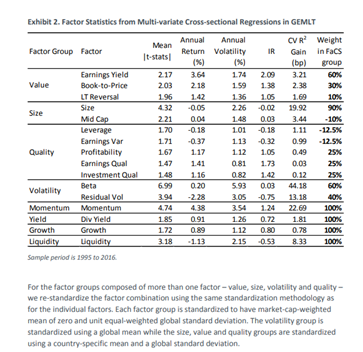

I have just found a statistics summary of different MSCI factors (based on the Barra Global Total Market Equity Model for Long-Term Investors (GEMLT)).

I wonder why the annual returns are so low compared to Fama-French-Factors. Does anybody have an idea why? I think that these factor returns are excess returns in case of the risk free rate, but this does not explain these low returns. I mean factor indices of MSCI deliver more than 11% p. a.

Link to the document of MSCI: https://www.msci.com/documents/10199/275765e9-d631-4222-b4aa-520f7fa7d830