I am reading about mathematical finance, and I was tipsed to ask the quesiton on this site. It is about the "law of one price".

Just first I'll make precise the model my book uses:

I have a single period, so I only have time t=0 and t=1.

$B_t$ is the bank account process, where $B_0=1$, and $B_1 \geq1$ is a stochastic variable.

The price process is $S=\{S_t: t=0,1\}$, where $S_0=(S_1(0),,.S_N(0))$ is the starting price for each security, and $S_1=(S_1(1),,...,S_n(1))$ are stochastic variables giving the end price.

$H=(H_0,..H_n)$ gives the trading strategy($H_0$ is just the starting money in the bank, and each $H_i$ is just the number of shares). So the value(it is a stochastic variable when t=1) is:

$V_t=H_0*B_t+\Sigma H_i*S_n(t)$.

This is the model the book uses.

Now comes the definition of the "law of one price":

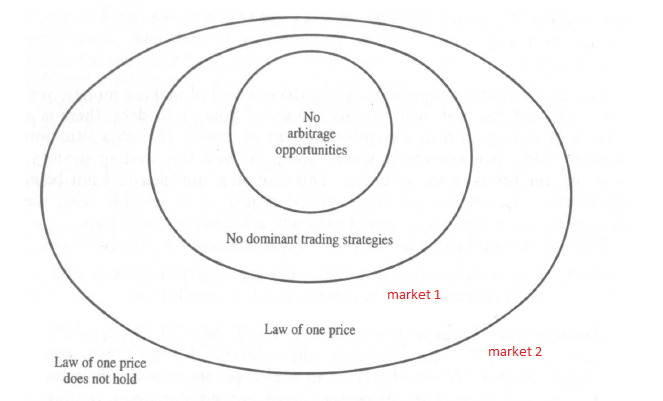

However I struggle to see why this is intuitive. I know that if this law don't hold we have arbitrage or a dominant strategy, so I've seen explanations that says if the law of one price doesn't hold, then we have arbitrage, and hends it is an illogical market.

However, I am wondering if the point of the "law of one price" can be explained without using "arbitrage" or "dominant trading strategies".

For instance like this figure shows, we may have two markets where we have arbitrage or dominant trading strategy, but where in one we have the law of one price, and in the other we don't have the law. How would you in this case explain that the law of one price gives a more realistic market?(you can not explain it with arbitrage or dominant trading strategy in this case).

PS: I know very little about finance terms, so i would really appreciate it if you explained in terms of the model I wrote in the start.