I will try and give some feedback on your questions.

- Will betas be negative for the short book?

Not necessarily, no. The beta of a stock is not related to you having a long or a short position to it.

- How would I calculate returns for the L/S portfolio

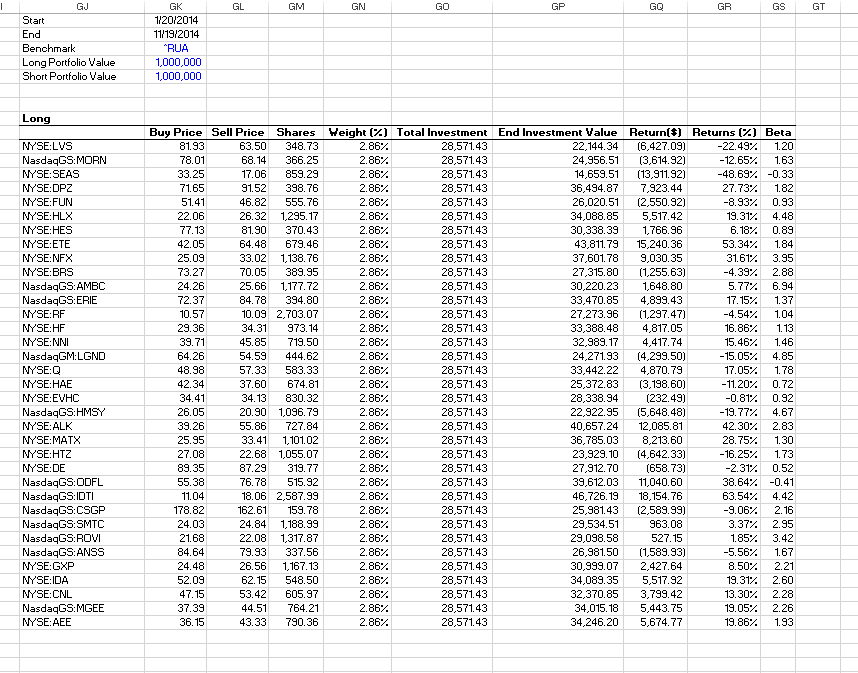

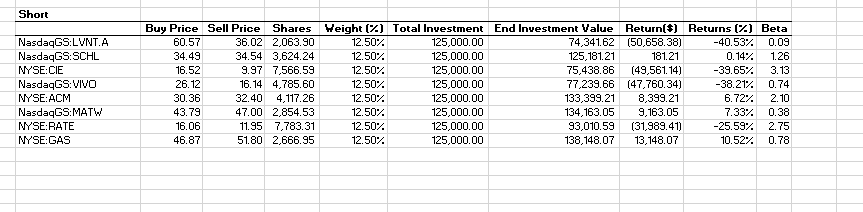

Assuming your total portfolio including cash is $V_{0}$, and each line has made $PNL_{i}$, then your long book ($L$) would make $P_{L}=\sum_{i \in L} PNL_{i}$ and your short book ($S$) $P_{S}=\sum_{i \in S} PNL_{i}$. Your total return would be $\frac{V_{0}+P_{L}+P_{S}}{V_{0}}$. In your excel picture, I would devide the column GQ with the total portfolio value (I think it is 1M) and this would be each line's performance contribution. If you sum that, then you end up to your portfolio's return.

- How would you factor in margin/borrowing costs in a model like this?

I do not really know about this.

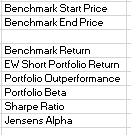

- Is there a different way that I need to calculate sharpe ratio since this is a L/S portfolio

Well the sharpe ratio is a function of the portfolio returns and its standard deviation, $S=\frac{R_{p}-R}{\sigma}$, where $R_{p}$ is your return, $R$ is the risk free rate, and $\sigma$ is your portfolio's standard deviation. So I don't think you need to change the computation. Most of the L/S hedge funds report on both Sharpe and Sortino ratio.

- How should I use the benchmark (I have read elsewhere that the benchmark should be long for the long portfolio, short the same benchmark for the short portfolio, and then long a cash investment)?

I am a little puzzled with your suggestion. The aim of the benchmark is to compare your portfolio in total with the benchmark. It doesn't really matter if your longs are doing fine, so you are overperforming the benchmark. If your shorts are very bad you might be net negative. But you can certainly consider this to test your longs vs your shorts.

Hope this helps.