It is well known that the theta of call option is always negative. Also, the theta of (at the money call option) goes to infinity as the time approaches to the maturity. On the other hands, (ITM and OTM) call option has zero theta at the maturity. This can be easily checked by BS formula.

Here, i am wondering that the above fact also holds for other models (eg. CEV or advanced models).

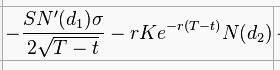

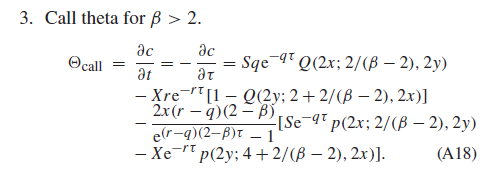

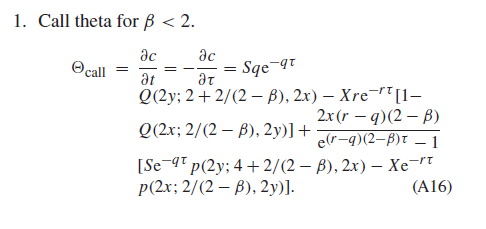

As i know, the theta of call option under CEV is given by

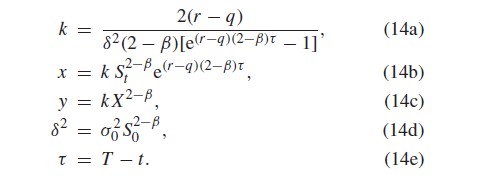

where

X is a strike price and $Q(w; v, λ)$ is the complementary distribution function of a non-central chi-square law with v degrees of freedom and non-centrality parameter λ.