I'm trying to build an automated forex trading system and I'm trying to understand how to calculate the number of units I should specify for each trade in different scenarios. Say for example I have an account with a broker in USD and I've deposited $1000. Ignoring leverage, I'd like to allocate my entire balance in each of the following scenarios. In each scenario I've tried to explain how I think the calculation should be performed..

Going Long

Long USD/JPY

Buy USD, sell JPY

USD is the base currency so units (USD) = 1000

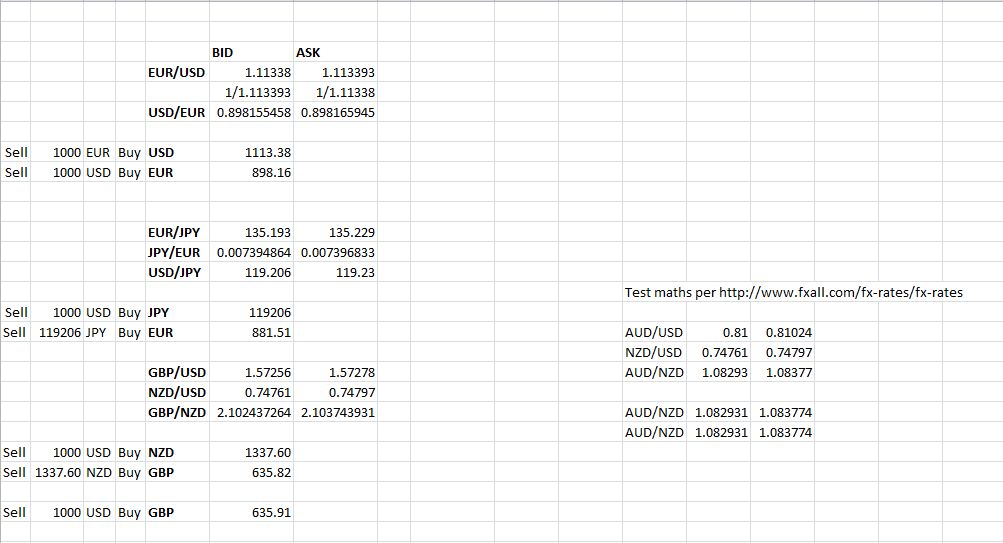

Long EUR/USD

Buy EUR, sell USD

units (EUR) = 1000 / [EUR/USD].Ask

Long EUR/JPY

Buy euros, sell yen

How many yen can we get with 1000 dollars?

Buy yen with dollars

Instrument = USD/JPY

USD (selling) is the base currency so multiply by the bid

So yen = 1000 * [USD/JPY].Bid

units (EUR) = yen * [EUR/JPY].Ask

Update:

units (EUR) = yen / [EUR/JPY].Ask

Long GBP/NZD

Buy GBP, sell NZD

How many NZD can we get with 1000 USD

Instrument = NZD/USD

USD (selling) is the quote currency so divide by the ask

So NZD = 1000 / [NZD/USD].Ask

units (GBP) = NZD / [GBP/NZD].Ask

Going Short

Short USD/JPY

Sell dollars for yen

units (USD) = 1000

Short EUR/USD

Sell euros, buy dollars

units (EUR) = 1000 * [EUR/USD].Ask

Update:

units (EUR) = 1000 / [EUR/USD].Bid

Short EUR/JPY

Sell euros, buy yen

How many euros can I buy with 1000 dollars?

Instrument EUR/USD

USD (selling) is the quote currency so divide by the ask

units (EUR) = 1000 / [EUR/USD].Ask

Short CHF/JPY

Sell CHF and hold JPY

How much CHF can we buy with 1000 USD?

Instrument = USD/CHF

USD (selling) is the base currency to multiply by the bid

units (CHF) = 1000 * [USD/CHF].Bid

So the question is - have I got the logic right in each scenario?

[ This is a follow up question to my previous question - Calculating units in a cross currency short trade ]