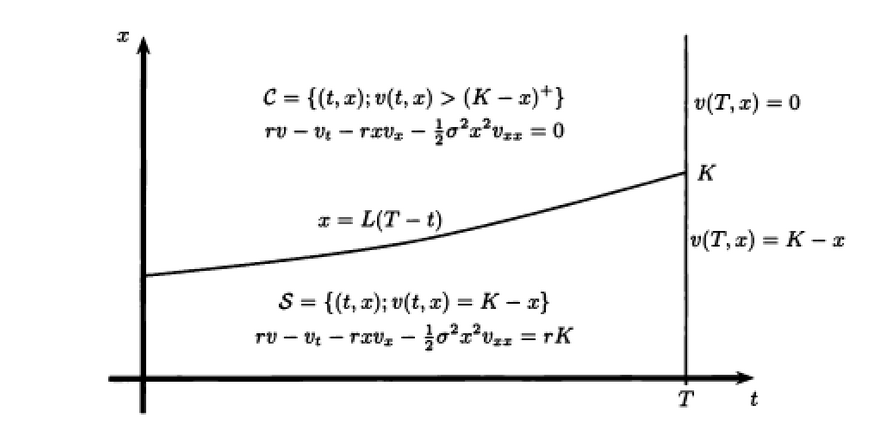

In the Black-Scholes Model or Heston Model, the American option satisfies the same PDE, but with different boundaries.For an American call option $C_A(S,\tau )$, we can therefore write

\begin{align}

\frac{\partial {{C}_{A}}}{\partial \tau }=+\frac{1}{2}{{\sigma }^{2}}{{S}^{2}}\frac{{{\partial }^{2}}{{C}_{A}}}{\partial {{S}^{2}}}+(r-q)S\frac{\partial {{C}_{A}}}{\partial S}-r{{C}_{A}}

\end{align}

or(Heston) $C_A(S,v,\tau )$ satisfy

\begin{align}

\frac{\partial {{C}_{A}}}{\partial \tau }=\,+\frac{1}{2}v{{S}^{2}}\frac{{{\partial }^{2}}{{C}_{A}}}{\partial {{S}^{2}}}+\rho \sigma \,vS\frac{{{\partial }^{2}}{{C}_{A}}}{\partial S \partial v}+\frac{1}{2}{{\sigma }^{2}}v\frac{{{\partial }^{2}}{{C}_{A}}}{\partial {{v}^{2}}}-rC_A+(r-q)S\frac{\partial {{C}_{A}}}{\partial S}+\kappa (\theta -v)\,\frac{\partial {{C}_{A}}}{\partial v}

\end{align}

where $\tau$ is the time until maturity. The PDE holds for $0 ≤ \tau < T$, where $T$ is the maturity calendar time, and for $0 < S ≤ b(v, \tau)$, where $b(v, τ )$ is the early exercise boundary. Essentially, this means that as long as the stock price is within the early exercise boundary, the American call option behaves like its European counterpart and the PDE holds.

Building on the work of Chiarella and Ziogas(2006), Tzavalis, and Wang(2003). approximate the early exercise boundary $b(v,\tau )$ with the log-linear function.

\begin{align}

b(v,\tau )=exp(b_0(\tau)+b_1(\tau)v)

\end{align}

They show the American call is obtained by adding the early exercise premium to the price of the European call

\begin{align}

C_A=C_E+V

\end{align}

where $V$ is the early exercise premium on an American call with strike $K$ and maturity is $\tau$