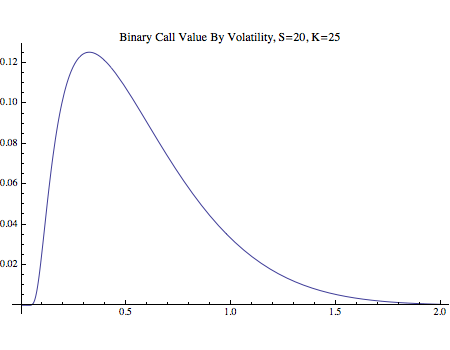

In theory, how should volatility affect the price of a binary option? A typical out the money option has more extrinsic value and therefore volatility plays a much more noticeable factor. Now let's say you have a binary option priced at .30 as people do not believe it will be worth 1.00 at expiration. How much does volatility affect this price?

Volatility can be high in the market, inflating the price of all options contracts, but would binary options behave differently? I haven't looked into how they are affected in practice yet, just looking to see if they would be different in theory.

Also, the CBOE's binaries are only available on volatility indexes, so it gets a bit redundant trying to determine how much the "value" of volatility affects the price of binary options on volatility.

{kind=link}