The SABR model of Hagan is described by the following Stochastic differential equations:

$$\begin{align}

& d{{f}_{t}}={{\alpha }_{t}}f_{t}^{\beta }d{{W}_{t}}^{1} \\

& d{{\alpha }_{t}}=v\,{{\alpha }_{t}}d{{W}_{t}}^{2} \\

& {{E}^{Q}}[d{{W}_{t}}^{1},d{{W}_{t}}^{2}]=\rho dt \\

\end{align}$$

In these equations, $f_t$ is the forward rate, $\alpha$ is the initial variance, $\beta$ is the exponent for the forward rate and $v$ is the volatility of variance.

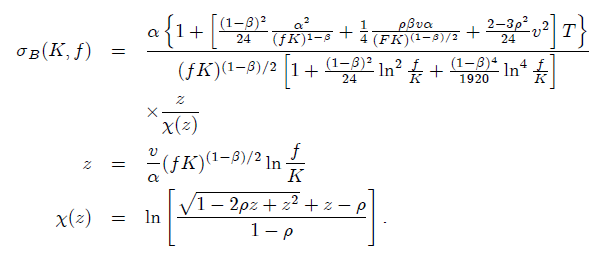

It is well-known the prices of European call options in the SABR model are given by Black's model. For a current forward rate $f$, strike $K$, and implied volatility $\sigma_{B}$ the price of a European call option with maturity $T$ is

$$C(f,K,{{\sigma }_{\beta }},T)={{e}^{-rT}}(f\,N({{d}_{1}})-K\,N({{d}_{2}}))$$

where

\begin{align}

& {{d}_{1}}=\frac{\ln \left( \frac{f}{K} \right)+\frac{1}{2}\sigma _{B }^{2}T}{{{\sigma }_{B }}\sqrt{T}} \\

& {{d}_{2}}=\frac{\ln \left( \frac{f}{K} \right)-\frac{1}{2}\sigma _{B}^{2}T}{{{\sigma }_{B }}\sqrt{T}} \\

\end{align}

and

Estimating $\alpha$, $\rho$ and v:

This can be accomplished by minimizing the errors between the model and market volatilities {$\sigma_{i}^{market}$}(from interest rate derivatives, for example) with identical maturity T. Hence, for example, we can use SSE, which produces

$$(\widehat{\alpha },\widehat{\rho },\widehat{v})=\underset{\alpha ,\rho ,v}{\mathop{\arg \min }}\,{{\sum\limits_{i}{\left( \sigma _{i}^{market}-{{\sigma }_{B }}({{f}_{i}},{{K}_{i}};\alpha ,\rho ,v) \right)}}^{2}}$$

Estimating $\beta$:

The at-the-money volatility $\sigma_{ATM}$ is obtained by setting $f = K$ in equation $\sigma (K,\beta)$, which produces

$${{\sigma }_{ATM}}={{\sigma }_{\beta }}(f,f)=\frac{\alpha \left( 1+\left[ \frac{{{(1-\beta )}^{2}}}{24}\times \frac{{{\alpha }^{2}}}{{{f}^{2-2\beta }}}+\frac{1}{4}\frac{\rho \beta v\alpha }{{{f}^{1-\beta }}}+\frac{2-3{{\rho }^{2}}}{24}{{v}^{2}} \right]T \right)}{{{f}^{1-\beta }}}$$

Taking logs produces

$$\ln {{\sigma }_{ATM}}\approx \ln \alpha -(1-\beta )\ln f$$

Edit for Gordon

In practice, the choice of $\beta$ has little effect on the resulting shape

of the volatility curve produced by the SABR model, so the choice of is not

crucial. The choice of $\beta$, however, can affect the Greeks. Barlett provides more accurate Greeks and shows that they are less sensitive to the choice of $\beta$.Indeed The case $\beta=0$ produces the stochastic normal model, $\beta=1$ produces the stochastic log-normal model, $\beta=\frac{1}{2}$ produces the stochastic CIR model.