In Pfaff's "Financial Risk Modelling and Portfolio Optimization with R" the following stylized facts are stated (among the others, p.26):

- The volatility of return processes is not constant with respect to time.

- The absolute or squared returns are highly autocorrelated.

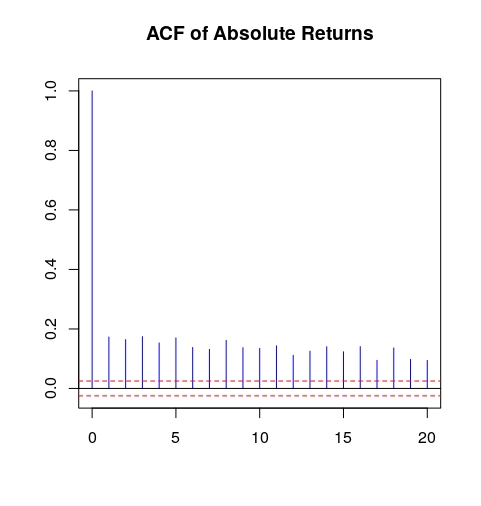

The following R code in the book is used to illustrate the latter of the above two claims:

library(fBasics)

library(evir)

data(siemens)

SieDates <- as.character(format(as.POSIXct(attr(siemens, "times")),"%Y-%m- %d"))

SieRet <- timeSeries(siemens*100, charvec = SieDates)

colnames(SieRet) <- "SieRet"

SieRetAbs <- abs(SieRet)

acf(SieRetAbs, main = "ACF of Absolute Returns", lag.max = 20,

ylab = " ", xlab = " ", col = "blue", ci.col = "red")

It generates the picture below:

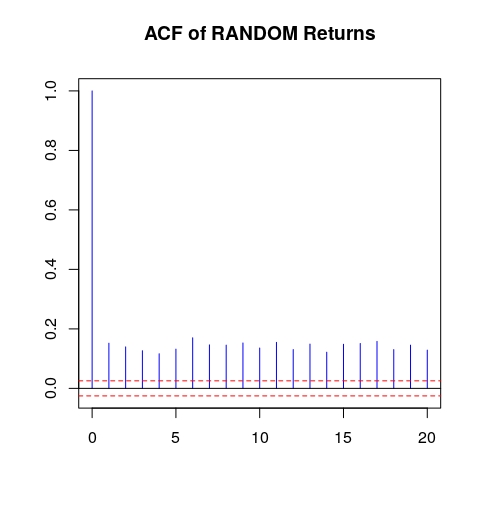

But a similar result can be achieved through introduction of single burst of volatility into the sequence of returns distributed normally with constant volatility as code below demonstrates:

Random <- do.call(c, lapply(c(0.8, 1.5, 0.8), function(x) rnorm(2000, sd=x) ) )

RandomAbs <- abs((Random))

acf(RandomAbs, main = "ACF of RANDOM Returns", lag.max = 20, ylab = " ", xlab = " ", col = "blue", ci.col = "red")

It generates the following:

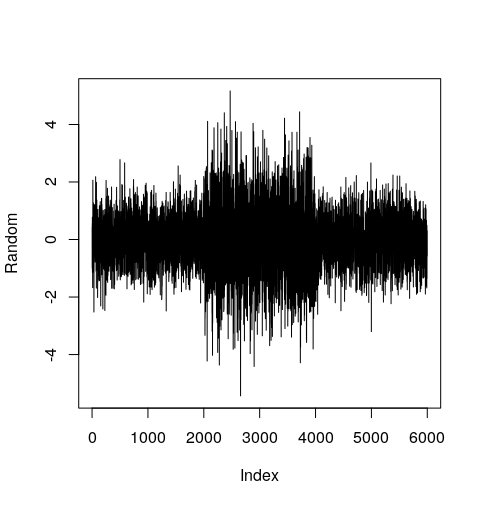

"Random" itself is shown below:

Can it be proven mathematically that such change in volatility will produce ACF of abs returns similar to the above? Is the opposite true?

In the Cont's article "Volatility Clustering in Financial Markets: Empirical Facts and Agent–Based Models" kindly shared with me by @JejeBelfort you may read:

A quantitative manifestation of this fact [volatility clustering] is that, while returns themselves are uncorrelated, absolute returns $|r_t|$ or their squares display a positive, significant and slowly decaying autocorrelation function: $corr(|r_t |, |r_{t+\tau} |) > 0$ for $\tau$ ranging from a few minutes to a several weeks.

But again why "Volatility clustering" implies positive autocorrelation of abs returns?

And will the returns where

large changes tend to be followed by large changes, of either sign, and small changes tend to be followed by small changes.

always produce ACF of abs returns similar to the above?