Preliminary

This answer provides evidence (and confirms your supposition!) that the HML factor in Germany is no longer rewarded with higher returns in the cross-section of German stocks. From July 1992 - December 2018, the average HML-premium is 0.49% (2.26) per month, but insignificantly -0.28% (-1.01) from July 2011 - December 2018. Momentum (WML) and operating profitability (RMW) are the most significant factors in Germany both in the total period (1,28% and 0.55% per month) and since 2011 (1,38% and 0.73% per month), whereas the investment style portfolio CMA may have its economic source in only some sup-portfolios or firms. Momentum and op. profitability are robust throughout the cross-section of German stocks.

Introduction

Fama/French (2015) test a five-factor asset pricing model that adds profitability and investment factors to the market, size, and value-growth factors of the Fama/French (1993) three-factor model. There is strong evidence that the size affect is not prevalent in integrated European markets and also reversed in some countries like Germany (Fama/French (2017) and Hanauer et al. (2011)). I replicated the Fama/French five-factor model for the German stock market and will extensively address this part of your question:

When i do the calculations for the sub-period from 2011 to 2018, i get a negative mean for the HML factor albeit with a statistically non-significant t-statistic (<0.5). Before that and for the entire period (1990-2018) i get a positive mean and a statistically significant t-statistic (>2). Can that be or am I doing something wrong?

Data

I use monthly financial data from Thomson Reuters Datastream and yearly accounting data from Worldscope from January 1990 - December 2018 for the German stock market. All data are denominated in euro and total returns (i.e. reinvesting dividends; adjustment for corporate equity activities) of any investment is assumed. To avoid the survivorship bias, all common stocks (stock type EQ, major flag Y, type of share C) including yet delisted stocks are considered in the sample. I start the stock selection with Worldscope lists (WSCOPEBD), dead lists (DEADBDX) and research lists (FGERX). Any financial company having SIC-codes between 6,000 - 6,999 is excluded prior to the analysis.

Data from Thomson Reuters Datastream has to be screened and corrected prior to any analysis. I follow Ince and Porter (2006) and Campbell et al. (2010) and exclude certain identifier within the company name to catch non-common stocks like ADR, REIT's or preferred shares. To mitigate the influence of tiny, illiquid stocks, i follow Ang et al. (2009) and exclude stocks with the lowest 5% of market capitalization or having an un-adjusted closing price lower than 1€ at the portfolio formation date. I apply the dynamic filters DS09 and DS10 from Schmidt et al. (2015) and set all return data to NA if it is greater than 990% per month

or if the return $r_t$ at the end of month $t$ is greater than 300% and $(1 + r_t)(1 + r_{t-1}) < 50%$ (we delete then both $r_t$ and $r_{t-1}$. Further, to mitigate the impact of outliers in accounting information, we winsorize all firm-level (accounting) ratios at the 1% and 99% levels at the portfolio formation date.

Fama-French Portfolios and the Momentum Factor

I follow Fama and French (1992), (1993) and (2015) and build portfolios at the end of each June. Firms with a negative book-value of equity are excluded and book-value of equity is defined as in Schmidt et al. (2015), i.e. i do not consider deferred taxes (unreported results are similar as what follows). With regard to OP, we do not include selling, general and administrative expense, as this item is not broadly available among international firms. The return predictability of operating profitability is, however, not affected by this adjustment. Momentum (WML) is the cumulative prior 12-month gross stock return, skipping the most recent month, see Jegadeesh and Titman (1993) and the WML definition on Kenneth French's data-library.

Summary statistics

A typical firm in our sample has a market capitalization of 1,228.35 million euro and a book-to-market ratio of 0.75. Typically, total assets growth with a rate of 24% per year and the operating profitability is 1.22. On average, there are 440 stocks with sufficient data to be included in the portfolio sort:

Table 1

Summary statistics for firm characteristic, July 1992 to December 2018

----------------------------------------------------------------------

Market Cap. B/M-Ratio Investment Profitabilty | N

1. Qu. 745.9 0.59 0.06 1.10 | 322

Median 1092.3 0.71 0.09 1.24 | 450

Mean 1228.4 0.75 0.24 1.22 | 440

3. Qu. 1413.1 0.87 0.21 1.38 | 534

Std. 604.2 0.23 0.36 0.19 | 111.71

Table 2 reports summary statistics for the factor returns of the Fama/French five-factor model for the German capital market:

Table 2

Summary statistics for monthly factor returns, July 1992 to December 2018

-------------------------------------------------------------------------

MKT SMB HML CMA RMW WML

Mean 0.53 -0.37 0.49 0.39 0.55 1.28

Std. 5.00 3.39 3.19 3.16 2.85 5.67

t-statistic 1.73 -2.09 2.26 1.83 3.11 4.36

-------------------------------------------------------------------------

This table reports average monthly returns, standard deviations of monthly

returns, and Newey and West (1987) adjusted t-statistics for the average

returns using a lag of six.

Over the sample period from 1992 to 2018, the average market premium amounts to 0.53% per month. All factor returns besides the market premium yield economically and statistically significant return premiums. Especially momentum is most relevant with an average premium of 1.28% per month in Germany.

The following Table reports the summary statistic for the sub-period 2011-2018:

Table 3

Summary statistics for monthly factor returns, July 2011 to December 2018

-------------------------------------------------------------------------

MKT SMB HML CMA RMW WML

Mean 0.51 -0.02 -0.28 -0.20 0.73 1.38

Std. 4.48 3.12 2.45 2.23 2.17 3.09

t-statistic 1.13 -0.07 -1.01 -0.68 2.81 5.36

-------------------------------------------------------------------------

This table reports average monthly returns, standard deviations of monthly

returns, and Newey and West (1987) adjusted t-statistics for the average

returns using a lag of six.

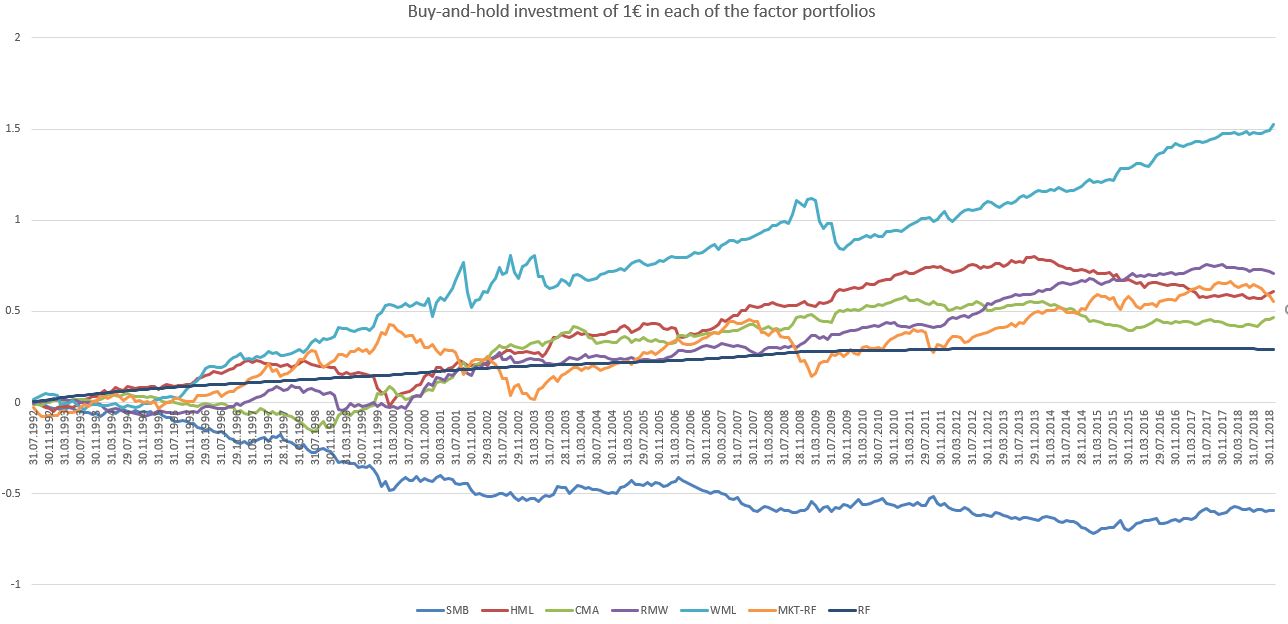

Comparing the total period to the sub-period of Table 3 shows, that the HML-factor reverses, but - carefully and precisely interpreted - becomes insignificant and not distinguishable from zero. The same interpretation holds for the CMA-factor return, while RMW remains its stability and WML both becomes statistical and economical larger. The following figure shows the growth of a buy-and-hold strategy, which invests 1€ at the end of June 1992 until December 2018 in each of the factor portfolios (with logarithmic ordinate):

As the figure shows, an initial investment of 1€ in the WML-portfolio results in a total portfolio wealth of 33.51€, whereas the SMB-investment results in a remaining 0.26€. Table 4 provides the total portfolio value of the initial buy-and-hold strategy starting in June 1992, as well as starting in June 2011:

Table 4

Buy-and-hold portfolio wealth of an initial 1€ investment in each factor portfolio

and the risk-free rate of interest RF

----------------------------------------------------------------------------------

Panel A: June 1992 - December 2018

Portfolio: MKT SMB HML CMA RMW WML RF

Total wealth: 3.60 0.26 4.07 2.94 5.07 33.51 1.96

Geom. return: 0.40 -0.43 0.44 0.34 0.51 1.11 0.21

Panel B: June 2011 - December 2018

Portfolio: MKT SMB HML CMA RMW WML RF

Total wealth: 1.45 0.94 0.76 0.82 1.89 3.29 1.01

Geom. return: 0.41 -0.07 -0.31 -0.22 0.71 1.33 0.01

Table 4 shows the strong prevalence of momentum in Germany, but together with the figure one can see that the momentum portfolio is largely hit by economic shocks and looses significantly in times of a crisis like the dotcom-crisis in the early 2000's or the financial-crisis in 2009. As already seen in Table 2 and Table 3, the HML-investment as well as the CMA-investment had negative performances after 2011.

Fama/MacBeth

Besides the non-parametric portfolio strategy in the previous section, i additionally apply the Fama/MacBeth (1973) regression approach. Table 5 reports the average coefficients (i.e. risk premia) of the following regression model:

$$r_{i,t+1} = \alpha_i + \beta_{i,t} + size_{i,t} + bm_{i,t} + inv_{i,t} + op_{i,t} + mom_{i,t} + \epsilon_t$$

where $\beta_{i,t}$ denotes the market beta of stock $i$, measured with monthly (excess) returns of the previous three years, i.e. 36 month with a minimum of 24 observations required, regressed on the monthly market premium. $size$ is the natural logarithm of firm size at the end of June $t$ and held constant until June of $t+1$. $bm$, $inv$, $op$ are the book-to-market ratio, the change in total assets and the operating profitability of a firm and updated yearly. $mom$ is the monthly updated gross return using 12 month and skipping the most recent month. I winsorize each month any independent variable on both sides on a level of 0.5% to mitigate the influence of outliers.

Table 5 presents the average coefficient estimates from monthly cross-sectional regressions of one month-ahead stock returns on the Fama/French risk-factor returns, firm beta and firm momentum for the total period of July 1992 to December 2018. All regressions are estimated using two different weighting schemes, equal-weights and value-weights. The equal-weighted cross-sectional regression approach corresponds to forming equal-weighted portfolios, whereas the value-weighted cross-sectional regression approach corresponds to forming value weighted portfolios. In summary, the value-weighting regression is based on the WLS-approach (weighted least squares) with the market capitalization of the previous month as weightings (see Asparouhova et al. (2013)):

Table 5

Cross-sectional regressions of one-month ahead stock returns on

Fama/French factor returns, firm beta and firm momentum from

July 1992 - December 2018.

-----------------------------------------------------------------

Panel A Panel B

Equal-weighted Value-weighted

-----------------------------------------------------------------

Intercept | 0.24 (0.85) -0.50 (-0.88)

Beta | -0.15 (-0.71) -0.16 (-0.48)

Size | 0.02 (0.47) 0.06 (0.90)

BM-Ratio | 0.12 (1.66) 0.64 (2.12)

Investment | -0.69 (-3.25) -0.02 (-0.06)

Op. Prof. | 0.06 (1.50) 0.15 (1.51)

Momentum | 1.42 (5.18) 1.04 (2.18)

------------------------------------------------------------------

t-statistics are provided in parenthesis and are Newey and West (1987)

adjusted using a lag of six.

Panel A of Table 5 provides evidence, that in an equal-weighted setting, the book-to-market ratio, Investment and Momentum have a strong influence on the one-month-ahead future stock return. In fact, firms with a high book-to-market ratio, high previous stock returns and low investments gain higher future returns. The value-weighted setting in Panel B shows, that the influence of investment diminishes, so the investment risk is strongly linked to small, tiny firms. The average size-premium is not significantly different from zero in both settings, although having a significant performance of -0.37% (-2.09) in the portfolio sort in Table 1. A more detailed analysis shows, that the size-effect is nearly completely located in the high performance of few large firms. While momentum has the most effect on return predictability, the market-beta of a firm is not significant.

Factor redundancy test

If a factor’s average return is captured by its exposures to the other factors in a model, that factor adds nothing to the model’s explanation of average returns and therefore can be dropped. In this section, i regress each of factors on the others to examine which return factor possesses unique information about expected returns and which factors may be redundant. The intercept in this regression provides the average return that is left unexplained by the exposures to the other five factors:

Table 6

Using five factors in regressions to explain monthly returns on the sixth

Panel A: July 1992 - December 2018

Dependent | MKT | SMB | HML | CMA | RMW | WML |

-----------------------------------------------------------------------

Intercept | 0.77 | 0.13 | 0.46 | 0.25 | 0.38 | 1.19 |

| (2.68) | (0.65) | (2.35) | (1.21) | (2.14) | (4.15) |

MKT | | -0.49 | -0.04 | -0.07 | 0.00 | -0.51 |

| | (-11.97)| (-0.49) | (-1.13) | (0.06) | (-3.90) |

SMB | -0.93 | | 0.00 | 0.00 | -0.01 | -0.43 |

| (-12.04)| | (0.01) | (0.01) | (-0.09) | (-3.35) |

HML | -0.05 | 0.00 | | 0.11 | 0.12 | -0.13 |

| (-0.50) | (0.02) | | (0.76) | (1.28) | (-1.01) |

CMA | -0.10 | 0.00 | 0.12 | | -0.08 | 0.41 |

| (-1.10) | (0.02) | (0.77) | | (-0.83) | (2.47) |

RMW | 0.01 | -0.00 | 0.15 | -0.10 | | 0.37 |

| (0.06) |-(0.09) | (1.40) | (-0.84) | | (2.12) |

WML | -0.25 | -0.11 | -0.05 | 0.15 | 0.11 | |

| (-5.25) |(-3.88) | (-1.01) | (2.31) | (2.55) | |

-----------------------------------------------------------------------

adj. R^2 | 0.51 | 0.45 | 0.02 | 0.10 | 0.05 | 0.23 |

-----------------------------------------------------------------------

Panel B: July 2011 - December 2018

Dependent | MKT | SMB | HML | CMA | RMW | WML |

-----------------------------------------------------------------------

Intercept | 0.70 | 0.47 | 0.11 | 0.09 | 0.67 | 1.56 |

| (1.17) | (1.31) | (0.42) | (0.32) | (2.58) | (4.08) |

MKT | | -0.48 | -0.14 | -0.10 | 0.08 | -0.33 |

| | (-7.00) | (-1.27) | (-1.62) | (1.14) | (-2.92) |

SMB | -0.93 | | -0.37 | 0.09 | -0.11 | -0.31 |

| (-5.96) | | (-2.76) | (1.01) | (-1.19) | (-2.90) |

HML | -0.23 | -0.32 | | 0.22 | -0.14 | -0.18 |

| (-1.21) | (-2.57) | | (3.90) | (-1.32) | (-1.74) |

CMA | -0.23 | 0.10 | 0.28 | | -0.21 | -0.03 |

| (-1.63) | (0.99) | (3.11) | | (-1.79) | (-0.19) |

RMW | 0.17 | -0.13 | -0.18 | -0.21 | | -0.09 |

| (1.03) | -(1.22) | (-1.34) | (-1.84) | | (-0.67) |

WML | -0.32 | -0.16 | -0.10 | -0.01 | -0.04 | |

| (-3.11) | (-2.32) | (-1.45) | (-0.19) | (-0.69) | |

-----------------------------------------------------------------------

adj. R^2 | 0.57 | 0.54 | 0.15 | 0.21 | 0.18 | 0.07 |

-----------------------------------------------------------------------

Dependent indicates the dependent variable in the regression. Newey and

West (1987) adjusted t-statistics for the coefficients are given in

parentheses. R^2 is adjusted for degrees of freedom.

As Table 6 shows, a linear combination of SMB, HML, CMA, RMW and WML is not able to generate the market risk premium, as 0.77% per month are left unexplained in the total period of July 1992 - December 2018. The SMB return however is strongly determined by the market premium and momentum. If the overall market moves 1% up in a month, the SMB return on average decreases 0.49%. The value-effect however is not rendered insignificant in presence of the other factor returns, as the intercept of 0.46% per month is significantly different from zero (t-statistic 2.35).

The sub-period of July 2011 - December 2018 (Panel B) provides evidence, that the HML (as well as SMB) return is subsumed by other risk premiums. The HML risk-factor is mostly explained by the SMB-return and CMA-return, left only an insignificant intercept of 0.11% (0.42) per month. This is interesting, because both SMB and CMA also may not add information about expected returns beyond that provided by the simultaneous influence of other factor risk premia. For this subperiod, the RMW and WML return are the only ones, which can not be explained by other factor returns.

Conclusion

I provide evidence that the Fama/French five-factor returns on the German stock market capture certain risk exposures in the total period of 1992-2018. Firm characteristics like size, book-to-market ratio, investment style and operating profitability are valid proxies for the exposure towards latent risk factors, which are cross-sectionally highly correlated with these firm-level variables. In contrast to the USA, the size effect in Germany is reversed, i.e. large stocks outperform small stocks.

The ability to capture risk-exposures however weakens in recent time. The value factor (HML) generates 0.49% per month overall, but an insignificant return of -0.28% per month since 2011. The only factors which are still highly significant (both statistically and economically) are WML and RMW, so momentum and operating profitability are strong risk exposures for German stocks. The parametric Fama/MacBeth (1973) regression shows, that the CMA return may have its economic roots in only some sub-portfolios rather than in the cross-section of the overall stock market.

References

Ang et al. (2009), High idiosyncratic volatility and low returns: international and further U.S. evidence. Journal of Financial Economics (91).

Asparouhova et al. (2013), Noisy prices and inference regarding returns. Journal of Finance (68).

Campbell et al. (2010), Multi-country event-study methods. Journal of Banking and Finance (34).

Fama/MacBeth (1973), Risk, Return, and Equilibrium: Empirical Tests, Journal of Political Economy, 81 (3).

Fama/French (1992), The Cross-Section of stock returns, The Journal of Finance 47(2).

Fama/French (1993), Common risk factors in the returns on stocks and bonds, Journal of Financial Economics 33(1).

Fama/French (2015), A five-factor asset pricing model, Journal of Financial Economics (116).

Fama/French (2017), International tests of a five-factor asset pricing model, Journal of Financial Economics (123).

Hanauer et al. (2013), Risikofaktoren und Multifaktormodelle für den deutschen Aktienmarkt (risk factors and multi-factor models for the german stock

market), Betriebswirtschaftliche Forschung & Praxis (65).

Ince/Porter (2006), Individual equity return data from Thomson Reuters Datastream: Handle with care!, Journal of Financial Research (29).