Disclaimer: Brand new to high frequency algo trading.

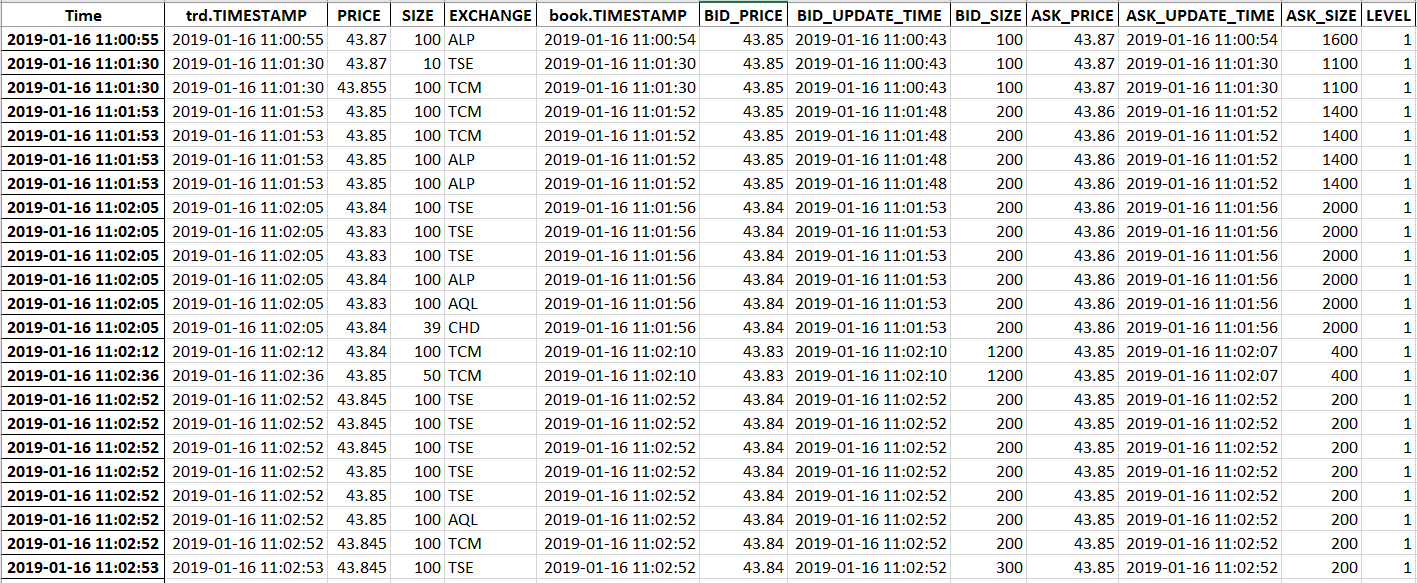

Background:I have tick-by-tick trade data for stock A and I have joined the price and volume data for each trade with the previous snapshot of the first level of the Quotes book table (i.e. BID and ASK snapshots). I thought this would be useful since you can see where the trade was lifted from (i.e. did it hit the bid or lift the offer?).

Question: Now I would like to simulate a trade execution (while assuming no market impact). In particular, assume I sit at 11:00:55 and my algorithm wants to place a buy order for 20 shares. How exactly would the execution algorithm play out? What's a simple conservative approach? In the case I'm considering, it's ok to wait a bit to execute the trade.

What I'm thinking: Look at the last trade as a reference price and put that price down on the BID side for 20 shares. Now passively wait to see if my BID was crossed for a few ticks, if not, increase the price a bit. Looking for some ideas from an expert or non-nube! Thank you.