I need some feedback on a very basic question regarding the calculation of the portfolio return.

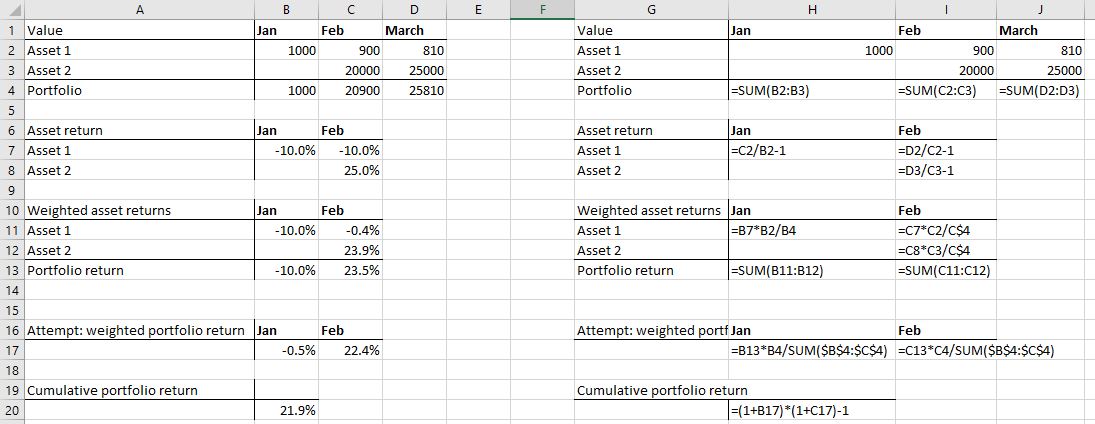

I have created an example of a portfolio with two assets and attempted to calculate the return:

I've calculated the weighted asset returns and from there I would like to calculate the cumulative portfolio return (= the return of the portfolio from Jan 1 to Feb 28). I can't just multiply them (1+r1)*(1+r2)-1, right? The -10% return in January was when the portfolio's value was only $1000 and the same relative decline in asset 1's value in February has a much smaller impact.

So do I simply weigh the returns according to the portfolio values? I've tried it and would appreciate some feedback on my calculation. Did I make a mistake? Is there an easier way to get the result?