What's the correct discount curve to use for exchange traded products? Would these be discounted at the OIS rate (because of the central clearing house)?

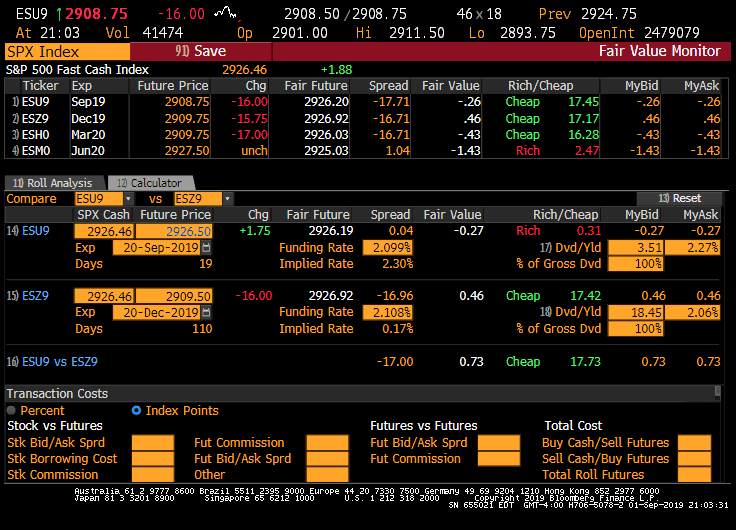

E.g. the E-Mini S&P500 Future @ CME: I'm trying to model liquidity preferences and implied dividends based on listed futures and options- so I need an accurate curve for the index's discounting. Some back-of-the-envelope tricks (treasury curves + basis) don't show enough structure in longer durations.

The S&P500 future is a unique market with its own characteristics. What about an equity forward curve with uncertain liquidity and dividends? Should I compute the repo cost (could be hard-to-borrow) of the stock from box spreads in order to discount the single equity (vs discounting the index)? Is there a better method in practice?

Collateralized OTC products are discount at OIS because this is the rate paid on the collateral. What about exchange products? What about equities with interesting financing characteristics?

Edit: is it the case that the financing I am giving up is the secured overnight rate for centrally cleared products when trading the index, so I should use the risk-free rate? What about for stock options with more interesting borrowing markets?