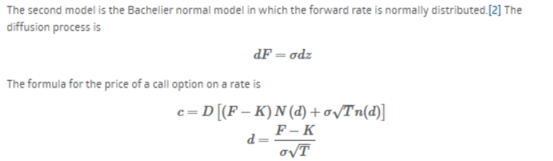

I am trying to estimate the value of a 0% interest rate floor by pricing each individual floorlet. Since BS won't work for this problem, I am trying to use normal volatility in a Bachelier model like the one proposed in this article:

Interest Rate Models and Negative Rates

To check my understanding, I priced a floor in Bloomberg and then downloaded the cash flows to see what vols and forwards the are using (BBG vol and model are set to 'Normal'). Unfortunately, my valuations are not even in the same ballpark. For example, for the nearest floorlet:

Notional: 100MM

Expiry: .24444yrs

Interest Period: .25556yrs

Libor Forward: 0.578%

Vol (Normal): 0.611%

So I get:

d=(0.00578-0)/(0.00611*sqrt(.2444))=1.8701

N(d)=.969268

n(d)=.069415

c=.005808, which needs to be multiplied by the notional and the day count to get the option premium

.005808 x 100MM x .2556=USD 14,843, which is way more than Bloomberg's price of $79.