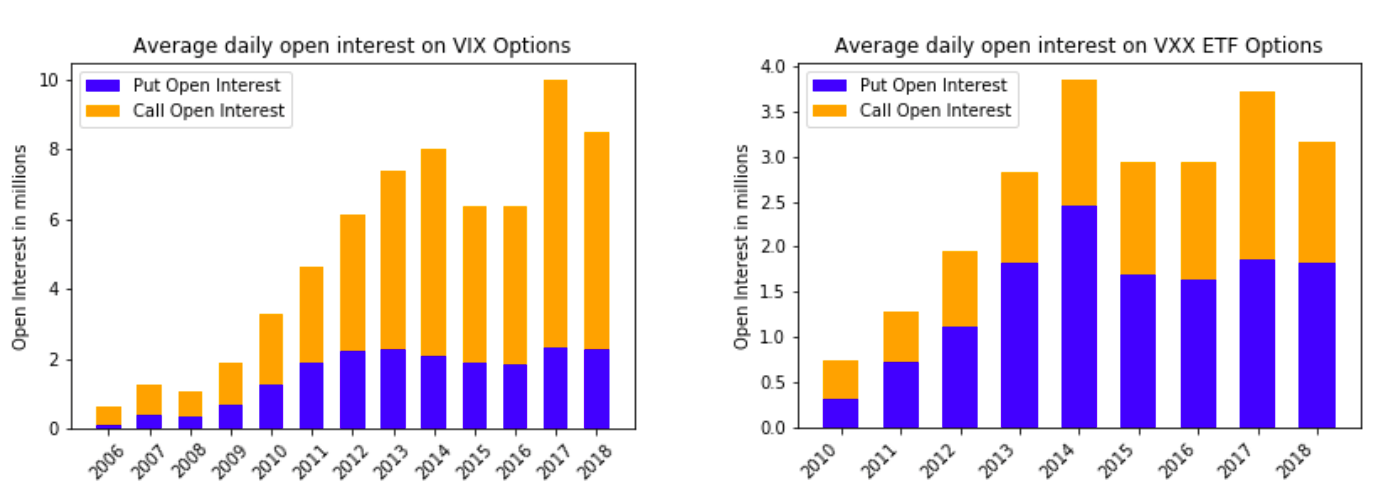

High open interest for a given option contract is an indicator for interest in that option. For that reason I wanted to take a look at how the open interest of options on volatility have evolved in the last years. To do so, I took a look at VIX options and options on the VXX (ETN on the VIX, options exist since 2010). Plotting the results in a stacked bar chart:

The growth of total open interest has been identical on the two types of volatility options. But the relation between call and put open interest is very different. Considering the close relationship between the VIX index and the VXX ETN, this comes as a surprise to me. Does anyone have a possible explanation or idea why the call/put open interest ratio is so different between the two?