So I am beginning to dabble my toe into quantitative finance and am trying to validate some model results and am having difficulty thinking about what they tell me.

Here's my situation: I'm trying to forecast returns using an ML model, and am experimenting with different window sizes for my training data, and am logging my n step ahead out-of-sample predictions. I'm also experimenting with an embargo.

So for example if my step is 2, and my embargo is 5, and my window size is 252, then X is 252 training observations, I would make a prediction for the next 2 observations (due to step), and there would be a gap of 5 observations between the training data and out-of-sample predictions.

Here's an abbreviated version of the formula I'm using, in python:

def walk_forward_validation(mod,

X,

y,

window = 504,

lookahead = 1,

step = 1,

embargo = 0):

"""

Parameters:

-- mod: model you are going to use for predictions

-- X : input data

-- y : target variable

-- window: size of training window you will use

-- lookahead: how many steps ahead will your model predict

-- step: how much additional data your model will move ahead after a round of fitting

-- embargo: how many samples to skip when making out of sample predictions

"""

start_idx = 0

stop_idx = window

pred_start = window + embargo

pred_stop = pred_start + lookahead

max_idx = X.shape[0] - 1

i = 0

# will store results in these, return as a df at the end

results = {

'preds': [],

'dates': [],

'true_vals': []

}

fitting = True

# start the training loop

while fitting:

# define the training window, fit the model

X_temp = X.iloc[start_idx:stop_idx]

y_temp = y.iloc[start_idx:stop_idx]

mod.fit(X_temp, y_temp)

# make future predictions, store the results

X_pred = X.iloc[pred_start:pred_stop]

# means we've gone past the cutoff point

if X_pred.shape[0] == 0:

break

results['preds'] += mod.predict(X_pred).tolist()

dates = X_pred.index.values.tolist()

results['dates'] += dates

results['true_vals'] += y.iloc[pred_start:pred_stop].values.tolist()

# update the new cutoffs

start_idx += step

stop_idx += step

pred_start += step

pred_stop += step

i += 1

# check to see if we've hit a new cutoff point

if stop_idx + lookahead > max_idx:

offset = (lookahead + stop_idx) - (max_idx - 1)

lookahead -= offset

results = pd.DataFrame(results)

results['dates'] = pd.to_datetime(results['dates'])

return pd.DataFrame(results)

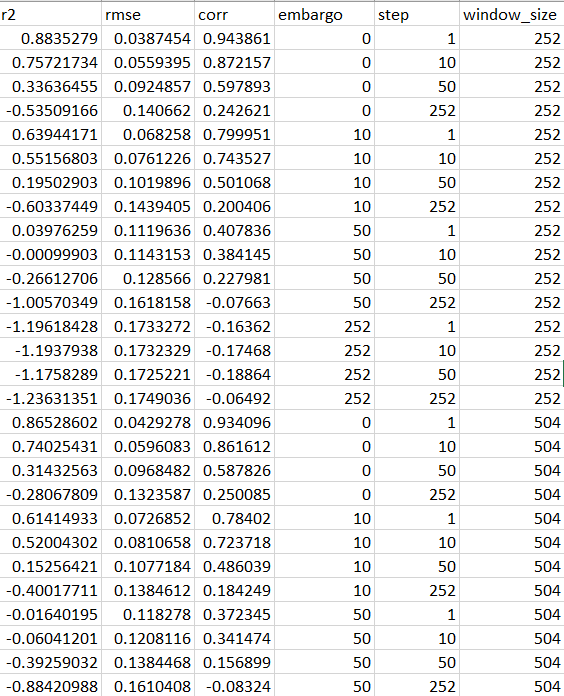

What I've done is looked at my model results for varying window sizes, step sizes, and embargo sizes.

Here's a table that summarizes the results:

What's obvious is that as embargo or step get bigger, the results deteriorate quickly. My take on this is that my model is probably highly sensitive to some very temporary patterns in my data that fade quickly, however I'm having a hard time figuring out the following issues:

- How should I choose which set of results to go by? Is there a particular reason one set of validation parameters is more likely to be stable than another? I know about stationary data, and have read Advances in Machine Learning about embargoing, but it's not clear to me that I should automatically choose the validation parameters that gave me the worst results. Let's assume my data doesn't have any look ahead biases.

- If I'm refitting my model on a regular basis to match the timespan of my out-of-sample predictions, is it then alright to go with the more optimistic validation parameters?

For example, let's suppose I'm fitting on hourly data with an embargo of 0 and step of 1. My results have an R2 value of 0.5. Even if these results are temporary in their nature, if I'm also refitting my model every hour, aren't I exploiting spatial correlations rather than being fooled by them?

I understand that results would decay quickly, but if I was unable to continually retrain the model on new data, I'll just stop it, knowing that disaster looms if I don't.

And lastly, is there anything fundamentally wrong with how I'm approaching this issue?

Thanks.

Anyways, sorry for the long post, just trying to get my head in the right place on these issues.

Thank you!