I am trying to simulate $n$ correlated geometric brownian motions (GBM) given a specified correlation matrix $\Sigma$ by following this procedure which uses Cholesky decomposition.

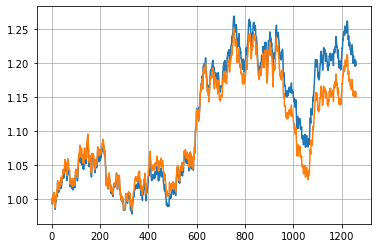

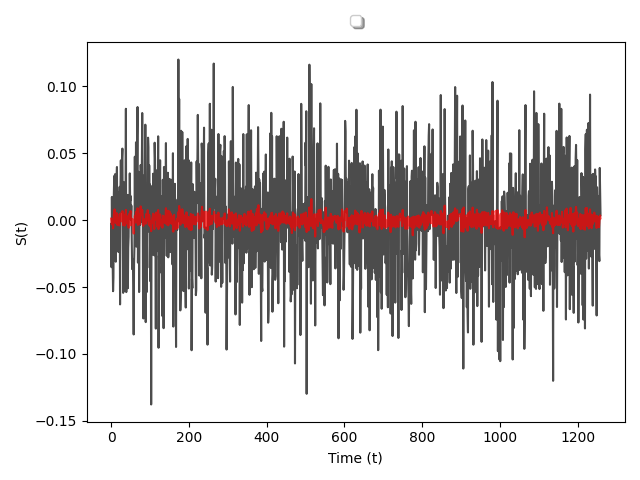

However, when I implement the code in Python one of the highly correlated ($\rho=0.99$) Wiener Processes have almost no volatility as can be seen in the plot below in the red line.

I would expect a correlation of $\rho=1$ to imply that the two processes would be identical and for $\rho=-1$, I would expect a "mirror" around 0.

The plot shows the realization of $W$ across $t$.

Note: In my attempt I try to avoid using any loops.

# PARAMETERS

n = 2 # number of assets

T = 5 # number of years

N = 252 # number of steps pr. year (T)

r = np.array([0.03, 0.03]) # drift-rate

q = np.array([0.0, 0.0]) # divivend-rate

S0 = np.array([1.0, 1.0]) # initial value

sigma = np.array([0.2, 0.2]) # diffusion-coefficients

corr_mat = np.array([[1.0, 0.99], [0.99, 1.0]]) # correlation-matrix

# Calculate step size

dt = 1 / (T * N)

# Vector of time index

t = np.array(range(N*T+1)).reshape((N * T + 1, 1)) * dt

# == PERFORM SIMULATION ==

# Draw normal distributed random variables

eps = np.random.normal(loc=0, scale=np.sqrt(dt), size=(N * T, n))

# Use Cholesky decomposition to get the matrix R satisfying: corr_mat = L x L^*

L = np.linalg.cholesky(corr_mat)

# Transform into realizations of correlated Wiener processes

W = eps @ L

# Calculate realizations of each stock as the realization of a GBM

# S_t = S0 * exp{ ((r-q) - ½sigma)*dt + sigma * W}

S = np.exp(

(((r - q) - np.power(sigma, 2) / 2) * dt).T + W * sigma.T

)

S = np.vstack([np.ones(S.shape[1]), S])

S = S0 * S.cumprod(axis=0)