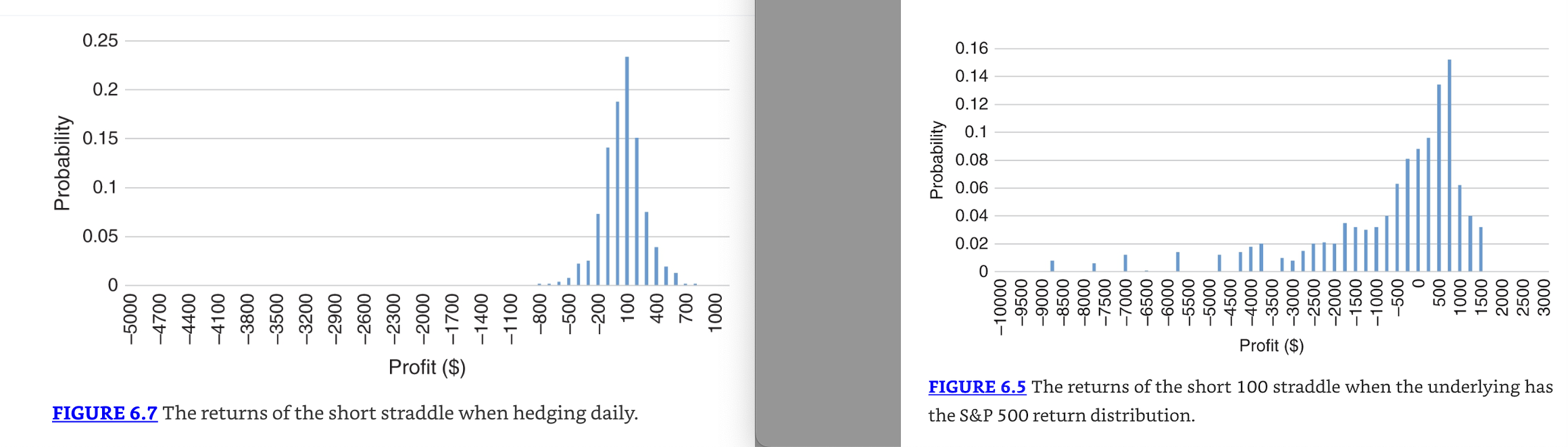

The information I have found about delta hedging frequency and (gamma) PnL on this site and numerous others all reiterate the same thing: that the frequency at which you delta-hedge only has an effect on the smoothness and variance of your PnL.

Nivel Egres: From the perspective of gamma pnl, the only thing that matters is the change in your asset price. Frequency is irrelevant - you can rebalance at different time periods or when delta exceeds a threshold or many other things - it is still an approximation of continuous integral and your expected P&L would be the same. For example, in real life, you are usually trying to optimize your hedging for a balance of (a) smoothness of P&L, (b) transaction costs, (c) vol dampening or amplifying (d) mean reversion found in the asset you're trading and (e) your risk limits.

How is this true though? Delta-hedging frequency has a direct effect on your PnL, and not just the smoothness of it.

So the thought here is that a trader who delta-hedges every minute, and a trader who hedges every end of day at market close, will both have the same expected profit at option expiry and only their PnL smoothness/variance will differ. Let's put this to the test.

We'll use this hypothetical scenario. And for the sake of simplicity we ignore transaction costs:

Two traders have bought a 100 strike ATM straddle (long gamma) that expires in a week on stock XYZ. The stock price is 100. They are both initially delta neutral. Throughout expiry, Trader A delta-hedges every minute, and trader B hedges every end of day at market close.

At 2:00 PM, stock XYZ drops -2% to 98. Trader A is delta-hedging the straddle every minute anyways so he buys shares to hedge and become delta-neutral again. The stock doesn't move at all until at 2:05 PM stock XYZ shoots up 4% from 98 to 101.92. Trader A sells the shares he previously bought, and then short sells some more shares to become delta-neutral. He has effectively locked in his gamma scalping PnL. The stock doesn't move at all again until 3:59 PM where the stock drops -1.88% from 101.92 to exactly 100. Trader A buys back his short shares, locks in his gamma PnL again, and is completely delta neutral.

Meanwhile it's the end of the day and time for Trader B to hedge, but he has nothing to delta-hedge because the stock is 100 at the end of the trading day, the same price at which he bought the ATM straddle and his delta of the position is 0.

Trader A has made some hefty PnL, meanwhile Trader B comes out with nothing at all and his missed out on volatility during the trading day which he could've profited off of had he been continuously hedging instead of just once a day.

So how does delta-hedging frequency just affect the smoothness and variance of PnL if we can clearly see it affects PnL itself in this example?