I can't understand a function which is part of a volatility model.

This is all explained in an open access paper titled "Volatility is (mostly) path-dependent" by Guyon and Lekeufack. My understanding after reading the paper is that we can model volatility as a simple regression of

$$ \sigma_t = \beta_0 + \beta_1 R_{1,t} + \beta_2 \sqrt{R_{2,t}} $$

The paper fits this equation on realized volatility (RV) and implied volatility (IV). This means that $\sigma_t$ is RV or IV and

$$ r_{t_i} = \frac{S_{t_i} - S_{t_{i-1}}}{S_{t_{i-1}}} $$

$$ R_{1,t} = \sum_{t_i \le t} K_1(t-t_i)r_{t_i} $$

and

$$ R_{2,t} = \sum_{t_i \le t} K_2(t-t_i)r_{t_i}^2 $$

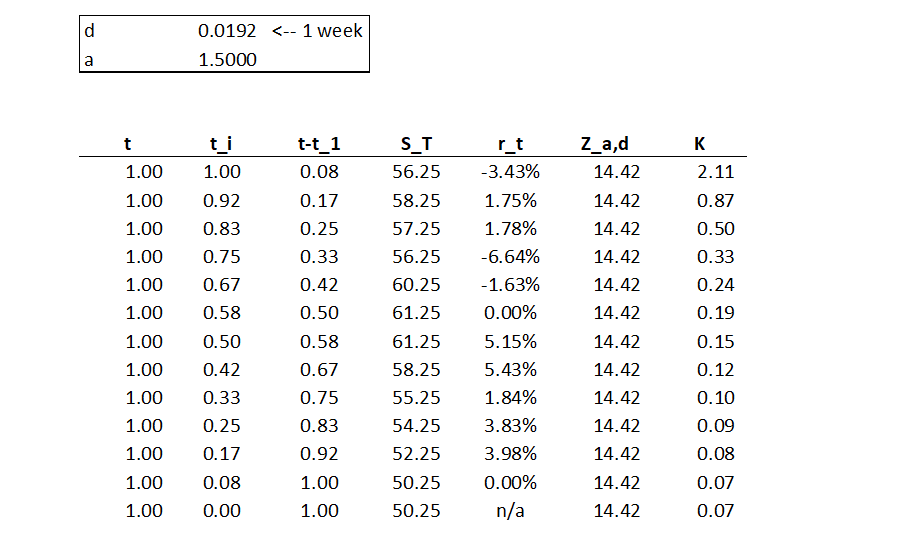

Now, $K_1(t)$ and $K_2(t)$ can be one of a number of decay function but the one the model uses is a time-shifted power law (see p. 8 of paper):

$$ K(\tau) = K_{\alpha, \delta}(\tau) = Z^{-1}_{\alpha, \delta}(\tau + \delta)^{-\alpha}, \quad \tau \ge 0, \quad \alpha > 1, \delta > 0 $$

where in the continuous time limit

$$ Z_{\alpha, \delta} = \int_0^\infty (\tau + \delta)^{-\alpha} d \tau = \frac{\delta^{1-\alpha}}{\alpha -1} $$

Now, I can't understand how to implement the $K(\tau)$ functions. I just don't understand what $Z^{-1}_{\alpha, \delta}(\tau)$ is and how to implement it numerically. Is $Z(t)$ connected to the normal distribution pdf?