Im working on the implementation of the Queue Reactive Model by Lehalle (https://arxiv.org/pdf/1312.0563.pdf), but I have encountered some implementation problems for my specific assets.

First, the average spread in them is between 15 up to 70 bps, a lot larger than tick size. In the paper, the reference price is updated by $\delta$ (tick size), but i think this would be a negligible change in my specific context. Maybe multiply by some constant?

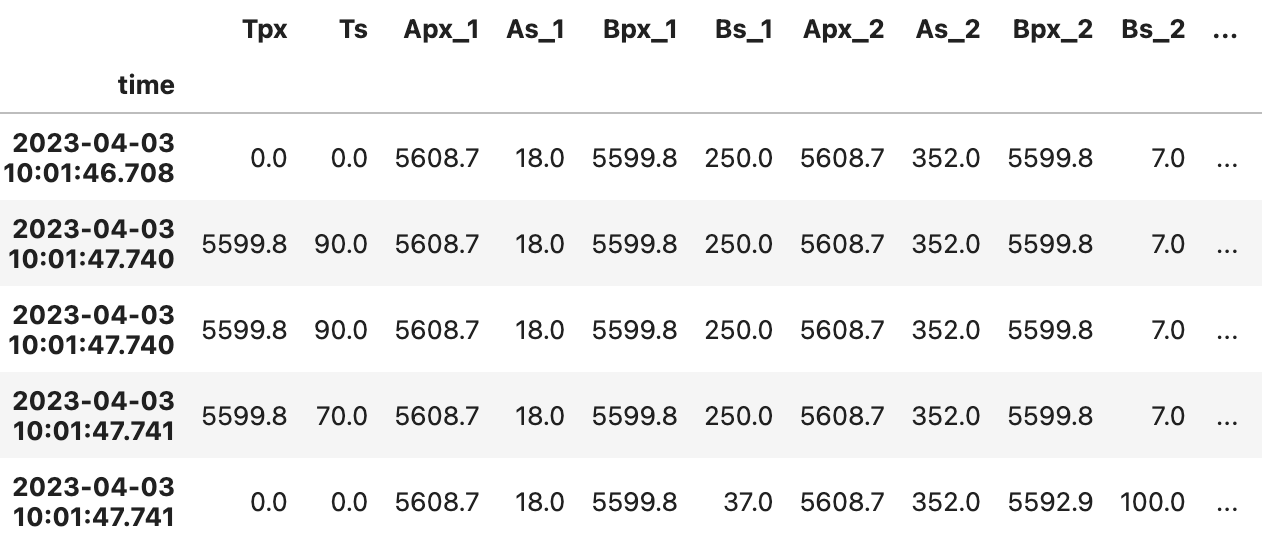

Second, my LOB data comes in this format (Incrementals, Up to level 5):

With $s$ meaning size. In this format, I can never have $q_{\pm 1} = 0$, making it difficult for the implementation of the intensities conditional on $q_{\pm 1} =0$ like in Model 2a. I dont know how i can overcome this problem.

Since I didnt find any code for this, I ventured to implement the paper on my own, but im struggling with the exact implementation for my assets and data. I would appreciate if someone can help me with this.

Thanks in advance