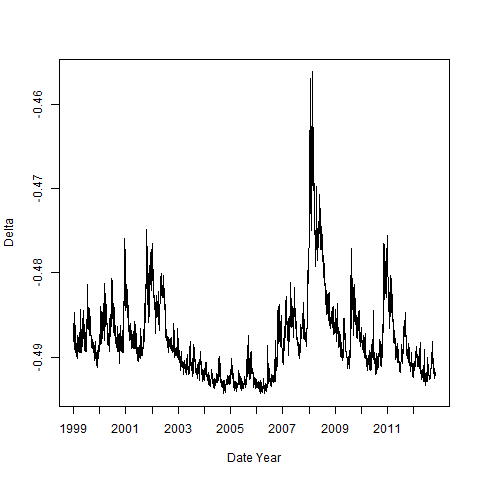

The plot below depicts the delta of a standardized at-the-money 30-day put option on the S&P500 tracker SPY over a 14-year period. This is data from OptionMetrics and standardized prices are calculated using linear interpolation from the volatility surface

My question is: Why does delta increase (i.e. decrease in absolute value) during the 2008 financial crisis?

Link: https://i.sstatic.net/0wtDm.jpg

{kind=link}

Delta of a put option over time, whose characteristics are constant. I.e. the underlying option characteristics is modeled so that it is perpetually at the money and 30 days from expiry