Where can I find more VaR and CVaR formulas for continuous distributions?

I collected a list here:

Where can I find more VaR and CVaR formulas for continuous distributions?

I collected a list here:

Values of VaR are just the inverses of the cumulative distributions.

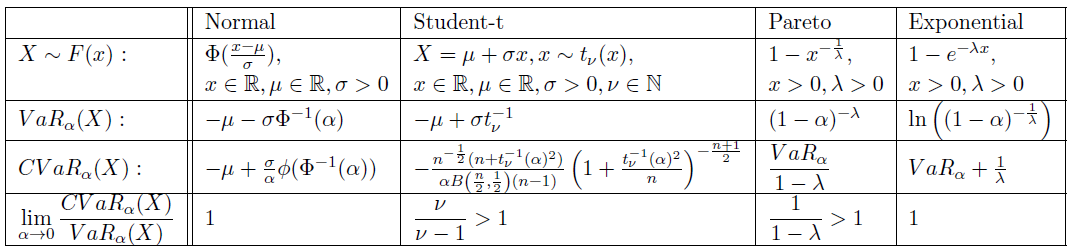

CVaR is not a very commonly used term, its more frequently used synonym is Expected Shortfall. See http://www.maths.manchester.ac.uk/~saralees/chap17.pdf for the list of Expected Shortfall values for more than 20 distributions.

More often than not, I prefer to work with a scenario representation. That is, I will simulate from the distribution and calculate the VaR and CVaR as appropriate. This is especially the case for forward-looking analysis of portfolios' CVaR, rather than in evaluating the historical returns of some portfolio.

If for some reason I can't do the scenario approach, then I will use the Cornish-Fisher approximation. There is a paper by Boudt, Peterson, and Croux that I think provides the formula for both VaR and CVaR, as well as a few others (perhaps refer to other references, and there's already a question on this site about it wrt VaR). If you're using Cornish-Fisher, then you can write the VaR and CVaR in terms of the moments of whatever distribution you're looking at. BPC provides the formula for portfolios as well, but in my experience this is a big pain.

The paper "Calculating CVaR and bPOE for Common Probability Distributions With Application to Portfolio Optimization and Density Estimation" by Norton, Matthew; Khokhlov, Valentyn; Uryasev, Stan (2018) gives a large number of CVAR analytical formula with full proof.

Most of them can also be found on the Expected shortfall (aka CVAR) Wikipedia page.