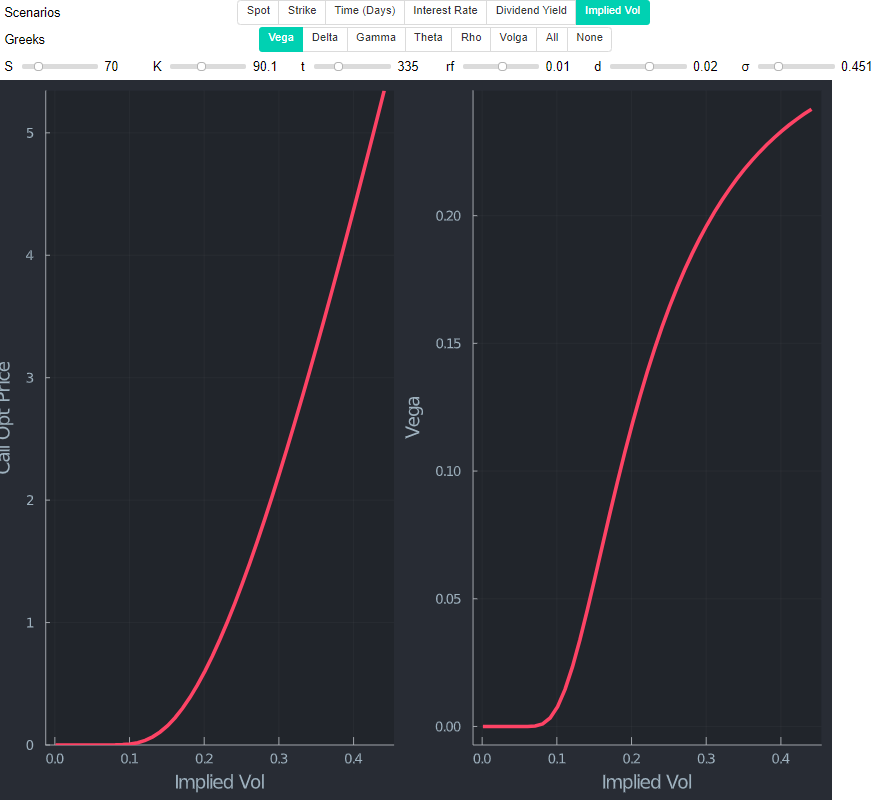

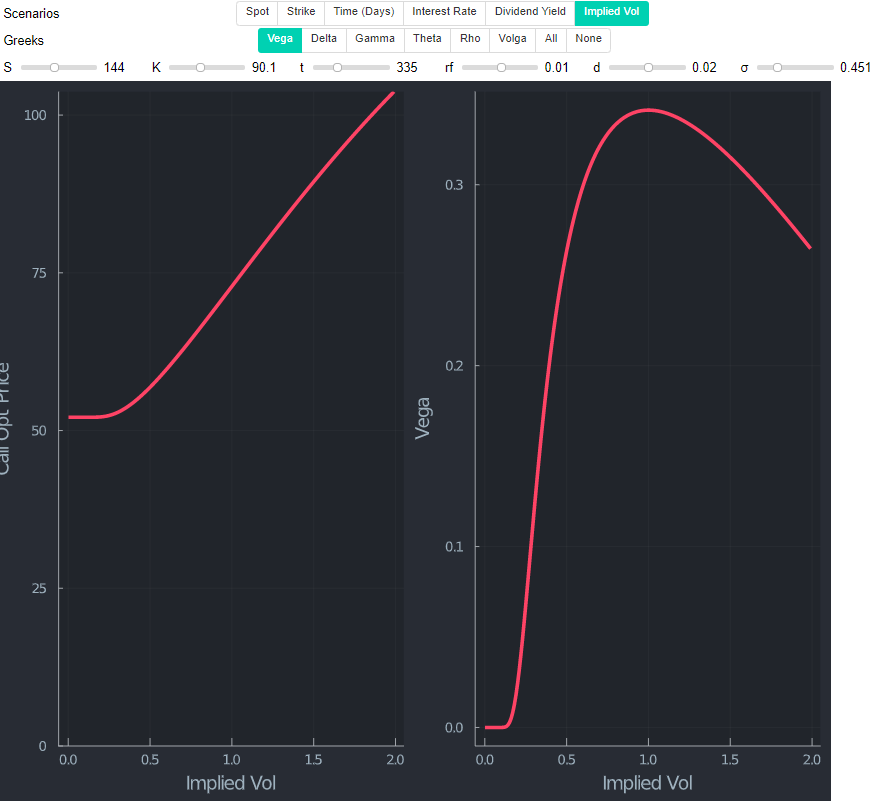

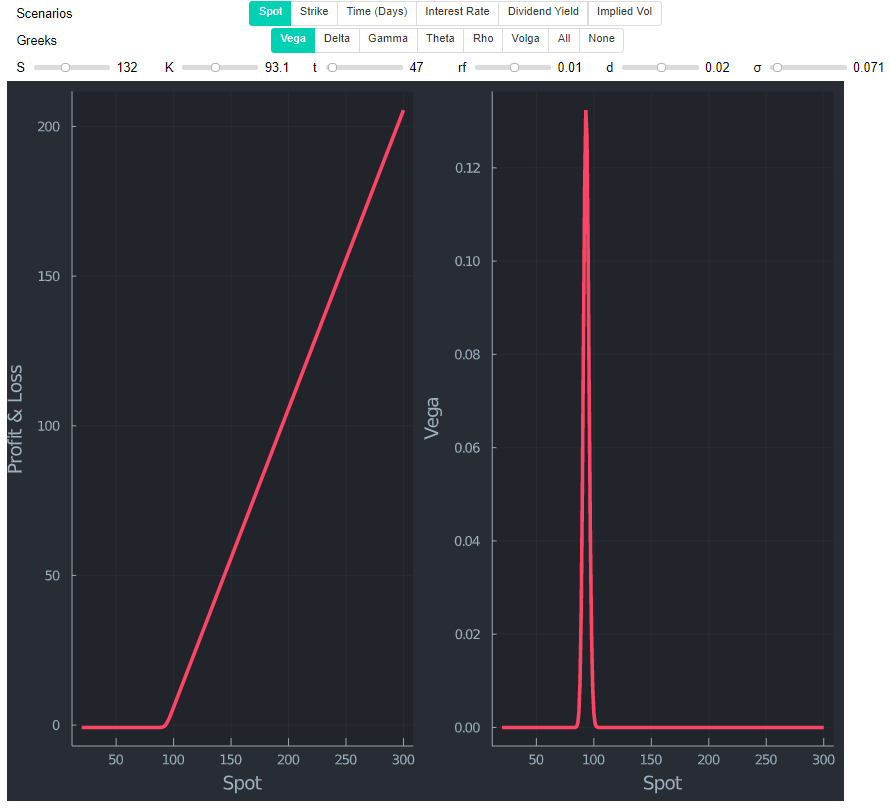

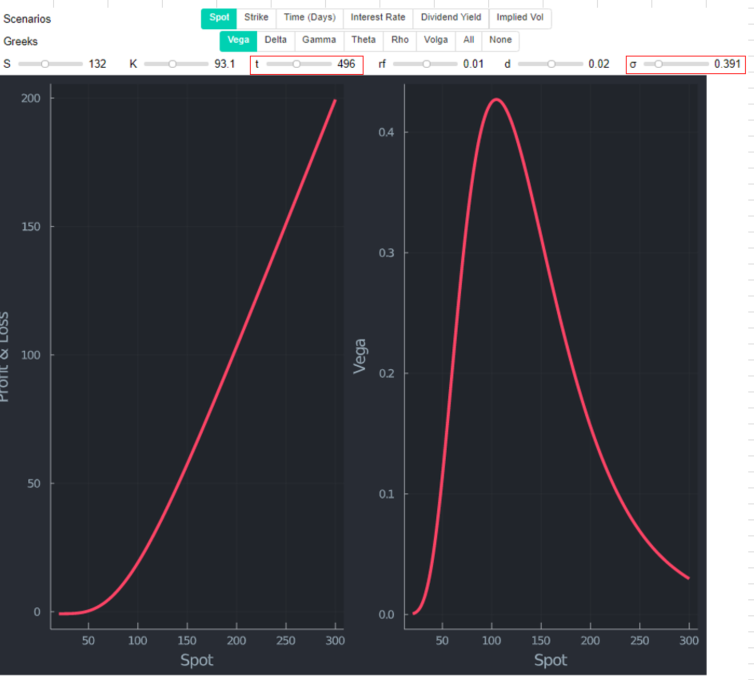

I've heard a question regarding pricing of european calls. The question is:

Is the call long or short in volatility when it is (deep) OTM? What is the profile of the implied volatility?

I know that in that case the answer is "long". Conversely the call would be short in vol if it was ITM.

I see a relation between long and the wish that volatility is high in order to go ITM if you hold the call. Also if you are ITM, I can see that your interest is to continue ATM. Therefore you want the volatility to be low.

I don't understand what exactly this term means neither where it comes from. I guess it is related to volatility trading/arbitrage.

Could someone please help me out and give me a precise definition for the term "long/short in volatility"?