How do you explain what a stationary process is? In the first place, what is meant by process, and then what does the process have to be like so it can be called stationary?

$\begingroup$

$\endgroup$

Add a comment

|

4 Answers

$\begingroup$

$\endgroup$

4

A stationary process is one where the mean and variance don't change over time. This is technically "second order stationarity" or "weak stationarity", but it is also commonly the meaning when seen in literature.

In first order stationarity, the distribution of $(X_{t+1}, ..., X_{t+k})$ is the same as $(X_{1}, ..., X_{k})$ for all values of $(t, k)$.

You can see whether a series is stationary through it's autocorrelation function (ACF): $\rho_k = Corr(X_t, X_{t-k})$. When the ACF of the time series is slowly decreasing, this is an indication that the mean is not stationary; conversely, a stationary series should converge on zero quickly.

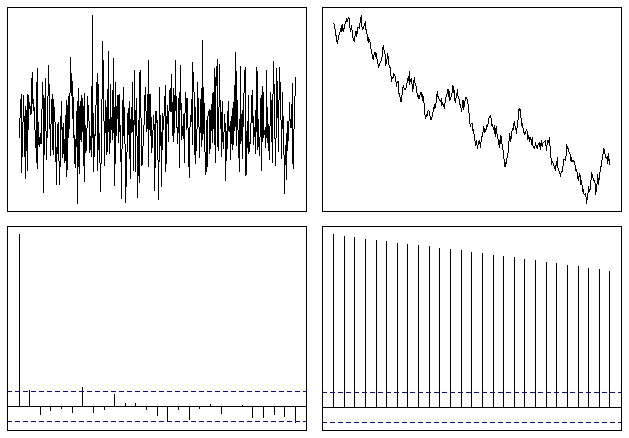

For instance, white noise is stationary, while a random walk is not. We can simulate these distributions easily in R (from a prior answer of mine):

op <- par(mfrow = c(2,2), mar = .5 + c(0,0,0,0))

N <- 500

# Simulate a Gaussian noise process

y1 <- rnorm(N)

# Turn it into integrated noise (a random walk)

y2 <- cumsum(y1)

plot(ts(y1), xlab="", ylab="", main="", axes=F); box()

plot(ts(y2), xlab="", ylab="", main="", axes=F); box()

acf(y1, xlab="", ylab="", main="", axes=F); box()

acf(y2, xlab="", ylab="", main="", axes=F); box()

par(op)

Which ends up looking somewhat like this:

If a time series varies over time, it is possible to make it stationary through a number of different techniques.

-

$\begingroup$ But you could have a stationary time series that is not independent, and an independent time series that is not stationary. $\endgroup$– PeteCommented Feb 7, 2011 at 20:43

-

$\begingroup$ I don't remember saying anything about independence... $\endgroup$– ShaneCommented Feb 7, 2011 at 20:44

-

2$\begingroup$ I mentioned it because I don't believe testing for stationarity through the behavior of the ACF is a good way to go, in general. I can understand that some people might work with series where an ACF test is sufficient. I just mean in general, I would not start with that. $\endgroup$– PeteCommented Feb 7, 2011 at 21:43

-

$\begingroup$ I just think that it's something visual which can be understood easily, which is why I provided it. $\endgroup$– ShaneCommented Feb 7, 2011 at 21:44

$\begingroup$

$\endgroup$

5

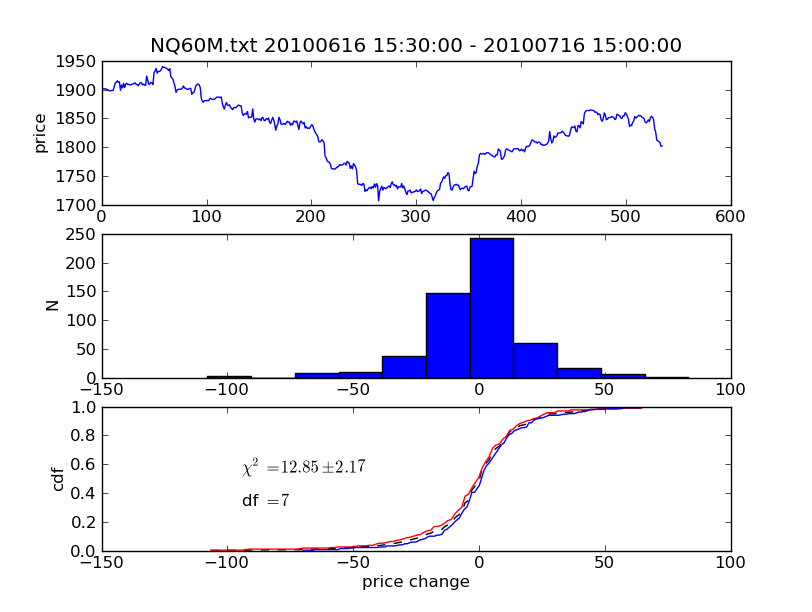

A very excellent discussion of stationarity as it relates to trading can be found in Sherry's (Sherrys'?) Mathematics of Technical Analysis (poorly organized, but very useful book). As he puts it, if the price changes of a stock, etc., are stationary over a time period, the underlying rules generating the price changes are effectively unchanged. The hypothesis is that a trading algorithm has little chance of working on a non-stationary series of price changes.

Below are some charts I've generated using the technique he describes in the book. Basically, you break your data set into two parts, histogram the prices changes, and construct cumulative distribution functions (cdfs). Then, do a Pearson's $\chi^2$ test to see if one cdf is significantly different than the other. You can also just look at the cdfs by eye. The case below is a borderline case. You can see the cdfs look a little bit different, but $\chi^2$ needs to be better than 14.07 to reach the 0.05 significance level in Pearson's test.

-

$\begingroup$ This reminds me of the Kolmogoroff-Smirnov test statistics. Among ohter things you can test with it if 2 series actually are coming from the same distribution (they both have to be iid samples though if I remember well). Anyway the wiki page is quit good in this topic. $\endgroup$ Commented Feb 5, 2011 at 22:28

-

$\begingroup$ Downvote and no comment.. curious.. $\endgroup$– PeteCommented Feb 10, 2011 at 16:33

-

$\begingroup$ Can you elaborate a bit on the technique? One CDF is for the price change, and the other is for what? Thanks! $\endgroup$– KostasCommented Feb 18, 2014 at 8:36

-

1$\begingroup$ Both CDFs are for price changes. In this case I used the first half vs. the second half of the series. $\endgroup$– PeteCommented Feb 18, 2014 at 18:41

-

$\begingroup$ You may find this wilmott thread on the book interesting, test process. He tries it on S&P which trends a lot. Can you apply the strategy to trending time series? $\endgroup$ Commented Apr 25, 2014 at 8:49

$\begingroup$

$\endgroup$

A process is defined here and is simply a collection of random variables indexed (in general) by time.

Otherwise I know the concept stated by Shane under the name of "weak stationarity", strong stationary processes are those that have probability laws that do not evolve through time.

More formally let $X_t$ be a given process, then let's call $P_X$ the probability law of the process, then for any given finite set of times $(t_1,...,t_n)$, and some borelian sets $(A_1,...,A_n)$ and any real $h>0$, $X_t$ is said (strongly) stationary iff :

$P_X(X_{t_1}\in A_1,...,X_{t_n}\in A_n)=P_X(X_{t_1+h}\in A_1,...,X_{t_n+h}\in A_n)$

For Gaussian process weak stationarity is equivalent to stationarity.

Regards

$\begingroup$

$\endgroup$

1

In mathematics and statistics, a stationary process (or strict(ly) stationary process or strong(ly) stationary process) is a stochastic process whose joint probability distribution does not change when shifted in time. Consequently, parameters such as the mean and variance, if they are present, also do not change over time and do not follow any trends.

-

1$\begingroup$ Any particular reason you are posting now? Your answer doesn't provide any new insight (IMO) and this question from 2011 already has an accepted answer. $\endgroup$– OlorunCommented Aug 1, 2015 at 14:09