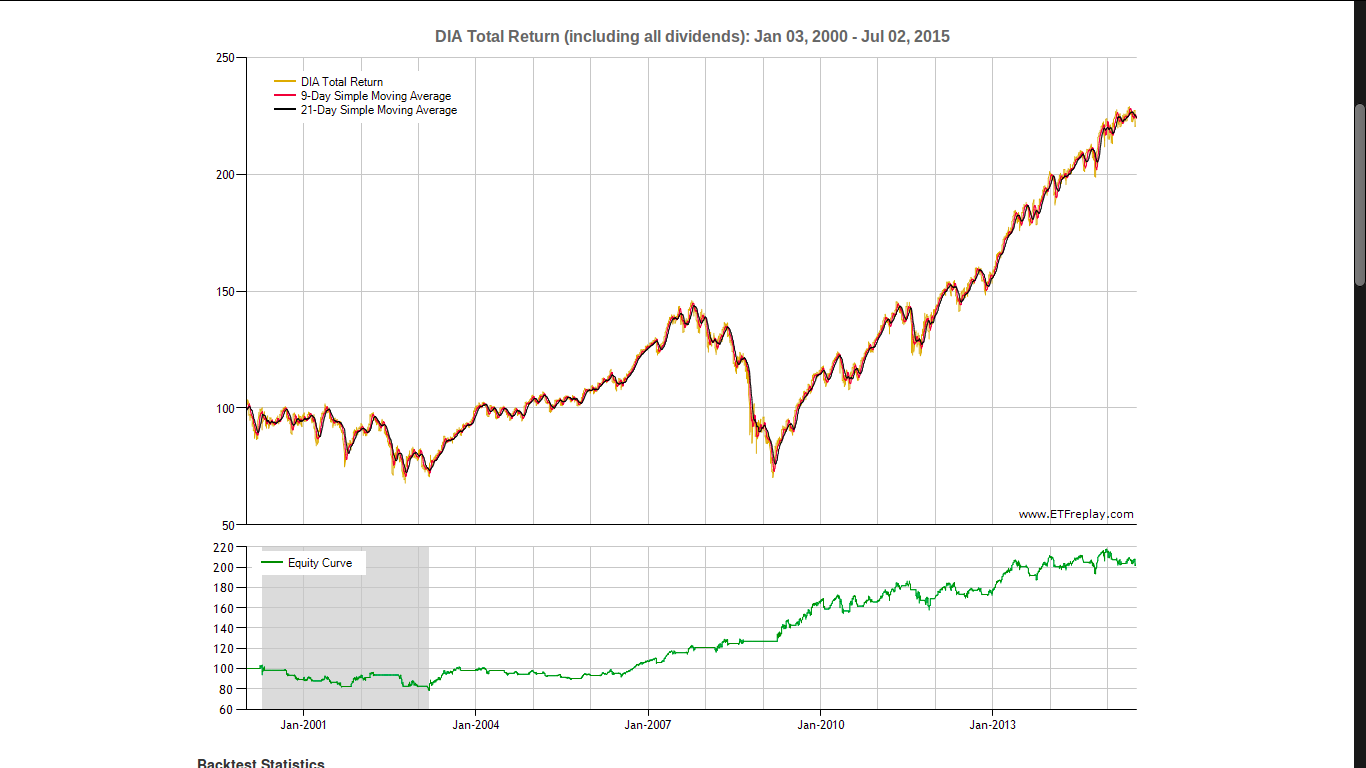

Moving average crossover strategy is a widely used strategy in algo trading. Is there a way to optimize return in a moving average crossover stratergy. I have used this site to backtest MA crossover stratergy in ETF's.

parameters used

ETF= DIA

MA Length=21 days(long),9 days(short)

Trade On= Day of cross

start date = 03-Jan-2000

end date= 02-Jul-2015

Advance setting= Default

Backtest statistics

Total Return= +62.7

Buy Sell Return Days In Trade

Mar 20, 2000 Apr 17, 2000 -0.76 20

May 23, 2000 May 26, 2000 -1.26 3

Jun 07, 2000 Jun 21, 2000 -3.08 10

Jul 11, 2000 Jul 31, 2000 -1.96 14

Aug 10, 2000 Sep 18, 2000 -0.65 26

Oct 31, 2000 Nov 20, 2000 -4.19 14

Dec 11, 2000 Dec 26, 2000 +0.15 10

Dec 28, 2000 Jan 17, 2001 -2.56 12

Jan 30, 2001 Feb 22, 2001 -2.68 16

Apr 11, 2001 Jun 05, 2001 +12.03 37

Jul 23, 2001 Aug 01, 2001 +1.34 7

Aug 03, 2001 Aug 08, 2001 -2.30 3

Oct 10, 2001 Jan 16, 2002 +5.44 67

Feb 12, 2002 Mar 28, 2002 +5.28 31

May 16, 2002 May 31, 2002 -3.68 10

Aug 07, 2002 Sep 05, 2002 -1.35 20

Oct 18, 2002 Dec 12, 2002 +3.32 38

Jan 08, 2003 Jan 24, 2003 -5.47 11

Feb 27, 2003 Mar 03, 2003 -0.57 2

Mar 20, 2003 Jul 01, 2003 +9.71 71

Jul 14, 2003 Aug 11, 2003 +0.78 20

Aug 12, 2003 Sep 29, 2003 +1.06 33

Oct 09, 2003 Oct 31, 2003 +1.04 16

Nov 04, 2003 Nov 20, 2003 -2.07 12

Dec 03, 2003 Feb 04, 2004 +6.11 42

Feb 12, 2004 Mar 04, 2004 -1.07 14

Apr 02, 2004 Apr 23, 2004 +0.02 14

Jun 02, 2004 Jul 07, 2004 -0.14 23

Aug 25, 2004 Sep 23, 2004 -1.30 20

Nov 04, 2004 Jan 10, 2005 +3.49 45

Feb 04, 2005 Mar 18, 2005 -0.60 29

May 06, 2005 Jun 28, 2005 +0.96 36

Jul 15, 2005 Aug 10, 2005 -0.05 18

Sep 12, 2005 Sep 23, 2005 -2.40 9

Oct 28, 2005 Dec 15, 2005 +5.02 33

Dec 23, 2005 Dec 30, 2005 -1.66 4

Jan 04, 2006 Jan 24, 2006 -1.54 13

Feb 08, 2006 Mar 10, 2006 +2.27 21

Mar 16, 2006 Apr 06, 2006 -0.31 15

Apr 21, 2006 May 19, 2006 -1.46 20

Jun 27, 2006 Jul 17, 2006 -1.59 13

Jul 31, 2006 Feb 28, 2007 +11.03 145

Mar 23, 2007 Jun 12, 2007 +6.97 55

Jun 21, 2007 Jun 27, 2007 -0.92 4

Jul 09, 2007 Jul 31, 2007 -3.04 16

Aug 31, 2007 Oct 22, 2007 +1.83 35

Dec 05, 2007 Dec 26, 2007 +0.96 14

Feb 06, 2008 Feb 15, 2008 +1.07 7

Feb 25, 2008 Mar 07, 2008 -5.29 9

Mar 26, 2008 May 21, 2008 +2.11 40

Jul 24, 2008 Aug 26, 2008 +0.63 23

Nov 04, 2008 Nov 14, 2008 -12.46 8

Dec 05, 2008 Dec 30, 2008 +0.42 16

Jan 06, 2009 Jan 15, 2009 -8.84 7

Mar 19, 2009 Jun 23, 2009 +13.41 66

Jul 20, 2009 Oct 06, 2009 +10.72 55

Oct 14, 2009 Nov 03, 2009 -2.33 14

Nov 11, 2009 Jan 25, 2010 -0.47 49

Feb 19, 2010 May 06, 2010 +1.50 53

Jun 17, 2010 Jul 01, 2010 -6.74 10

Jul 16, 2010 Aug 18, 2010 +3.52 23

Sep 09, 2010 Nov 19, 2010 +8.07 51

Dec 07, 2010 Mar 03, 2011 +8.46 59

Mar 29, 2011 May 19, 2011 +3.09 36

Jun 29, 2011 Jul 29, 2011 -0.99 21

Aug 31, 2011 Sep 14, 2011 -3.06 9

Sep 16, 2011 Sep 20, 2011 -0.85 2

Oct 13, 2011 Nov 21, 2011 +0.84 27

Dec 07, 2011 Apr 10, 2012 +4.97 84

Apr 26, 2012 May 11, 2012 -2.78 11

Jun 15, 2012 Aug 31, 2012 +3.22 54

Sep 11, 2012 Oct 10, 2012 +0.35 21

Nov 30, 2012 Apr 25, 2013 +13.92 99

Apr 30, 2013 Jun 06, 2013 +1.79 26

Jul 09, 2013 Aug 14, 2013 +0.48 26

Sep 12, 2013 Oct 03, 2013 -2.00 15

Oct 21, 2013 Dec 12, 2013 +2.76 37

Dec 23, 2013 Jan 22, 2014 +0.60 19

Feb 19, 2014 Mar 21, 2014 +1.76 22

Mar 28, 2014 Apr 14, 2014 -0.86 11

Apr 25, 2014 Jul 31, 2014 +1.75 67

Aug 20, 2014 Oct 01, 2014 -0.90 29

Oct 29, 2014 Dec 15, 2014 +1.67 32

Dec 29, 2014 Jan 13, 2015 -2.29 10

Feb 10, 2015 Mar 11, 2015 -0.94 20

Apr 15, 2015 May 06, 2015 -1.31 15

May 13, 2015 Jun 04, 2015 -0.63 15

Jun 23, 2015 Jul 01, 2015 -2.05 6

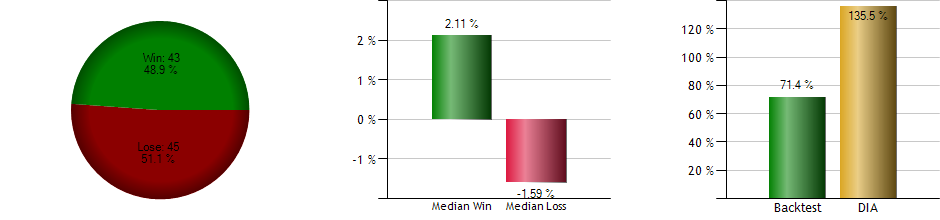

From the backtest data we can infer that the total return percentage of our moving average stragery is way lesser (71%) than the Benchmark DIA (135%). So how should we optimize our MA crossover algorithm to get a total return percentage equal or more than that of benchmark. How to prevent negative returns ?

example

Dec 29, 2014 Jan 13, 2015 -2.29 10

Feb 10, 2015 Mar 11, 2015 -0.94 20

Apr 15, 2015 May 06, 2015 -1.31 15

a way to prevent trades when return are in negative.

Consider this pseudo code as the MA crossover algorithm

initial_invest=1500 //initial investment amount

shareprice=15 // value of one share//

ma_short=9 // moving averages 9 days

ma_long=21

if ma_short crossabove ma_long

Buy share

elif ma_short crossbelow ma_long

sell share

endif