It is never optimal to exercise an american call option early if it is written on a stock that doesn't pay dividends, yet when pricing such an option, using a binomial model, we check whether or not it is optimal to exercise at each node.

I find it strange that it is never optimal to exercise early yet we take into account in its price the payoff from exercising early.

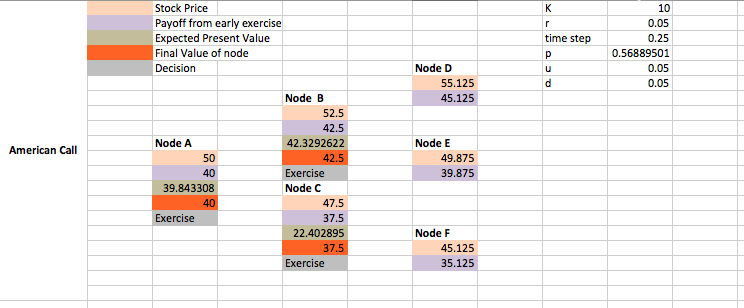

Does anyone know a good argument to explain this? Consider the following example of a call option

it is clearly optimal to exercise early everywhere, so it implicit in the question that the stock underlying the option pays dividends?