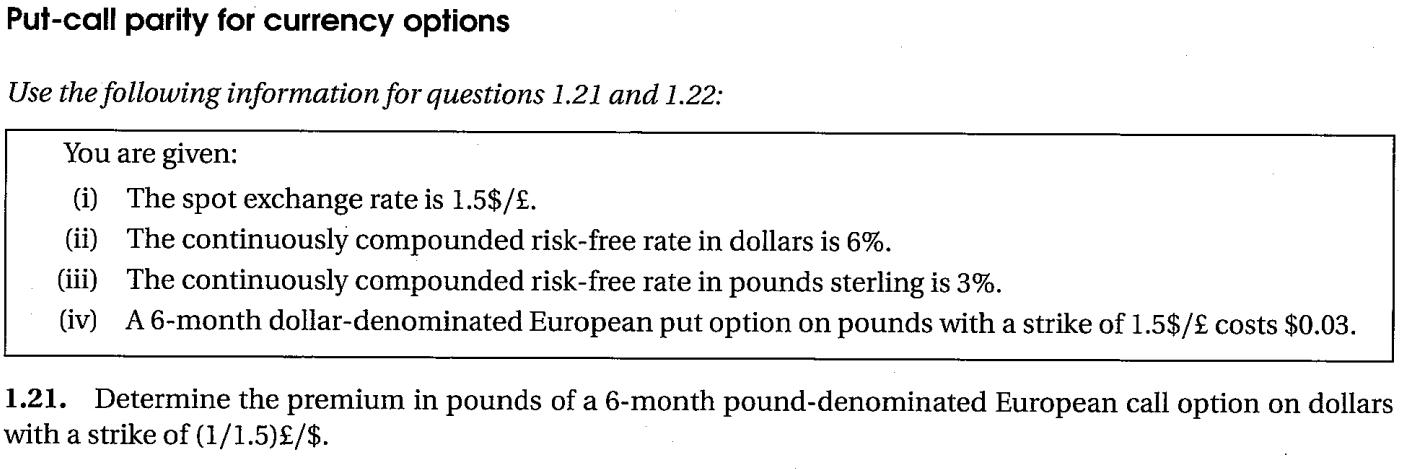

I am self-studying for an actuarial exam on models for financial economics. I am having difficulty thinking about the put-call parity for currency options, specifically how use the notation. Here is the problem:

My book uses the notation $C(x_0, K, T)$ to mean a call option on currency with a spot exchange rate $x_0$ to purchase it at exchange rate $K$ at time $T$, and $P(x_0, K, T)$ the corresponding put option.

Please tell me if my interpretation is correct:

I interpreted (iv) to mean $P(1 £, 1.5\frac{\$}{£}, 0.5) = \$0.03.$

I interpreted that the problem is asking us to find $C(1\$, \frac{1}{1.5} \frac{£}{\$}, 0.5)$.

The problem is that the first argument of those options do not appear to be rates.

This may not help, but by duality, $P(1 £, 1.5\frac{\$}{£}, 0.5) = C(1.5\frac{\$}{£}, 1 £, 0.5)$.

I don't see how to take what we're given, and convert to what the problem is asking us to find.