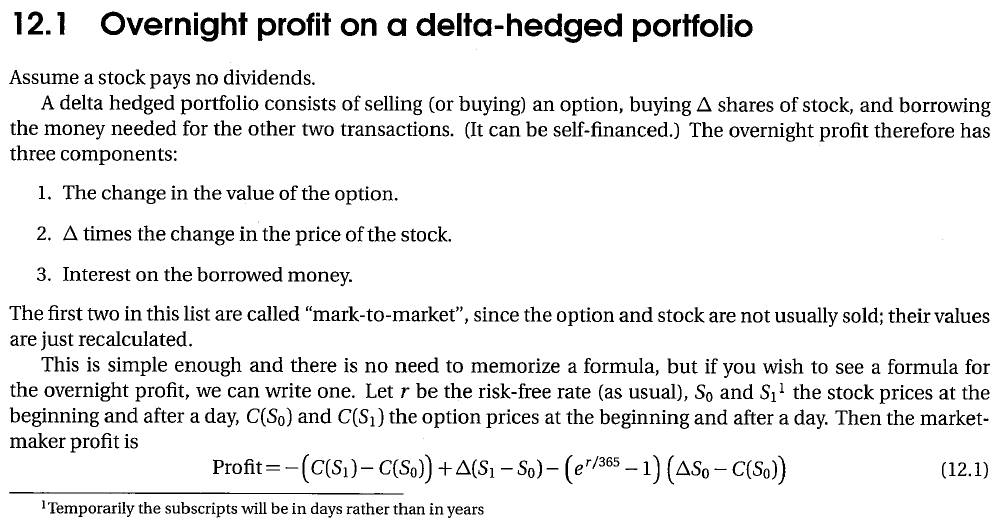

I am self-studying and encountered the following passage from my textbook on the market maker's overnight profit on a delta-hedged portfolio:

I don't understand why their isn't a factor of $(e^{r/365} - 1)$ multiplied by the $C(S_0)$ term. My reasoning is that if a call/put is sold, the positive cash flow from the premium could be invested at the risk-free rate.

My understanding is that the overnight profit on a sold call would be the premium that the call sold for at day 0, which could be invested at the risk free rate overnight, minus the premium that the call could be sold for if held on to for another day, or $C(S_0)\left(e^{r/365} - 1\right) - C(S_1)$

Wouldn't it be more accurate to say that: $$\text{Profit} = -\left(C(S_1) - C(S_0)(e^{r/365} - 1)\right) +\Delta(S_1 - S_0) - (e^{r/365} - 1)\left(\Delta S_0 - C(S_0)\right)?$$

If we're factoring interest lost on self-financing the selling of an option and buying $\Delta$ shares of stock, why wouldn't we also factor interest gained by selling the option at $T = 0$?