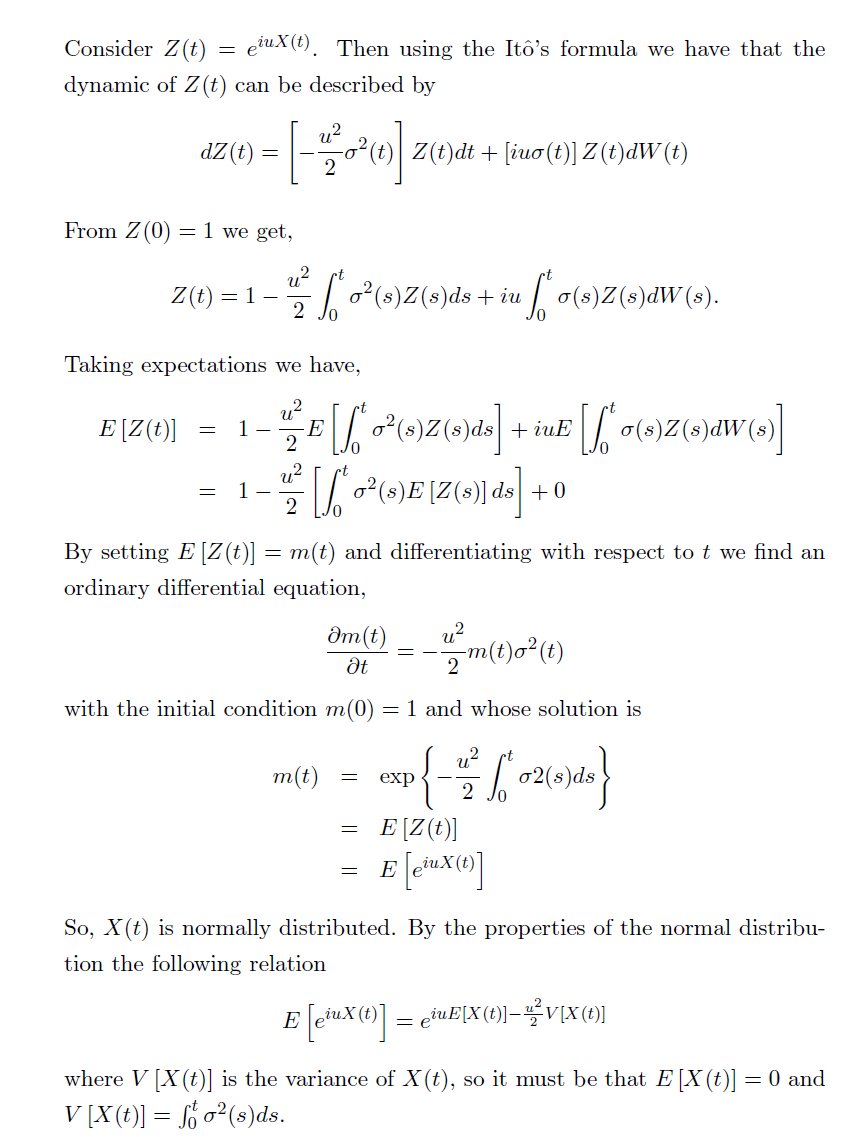

Some basic details

$\quad$ The Itô integral can be defined in a manner similar to the Riemann–Stieltjes integral, that is as a limit in probability of Riemann sums; such a limit does not necessarily exist pathwise. Suppose that $W_t$ is a Wiener process and that $\sigma_t$ is a right-continuous (cadlag), adapted and locally bounded process if $I=\{t_0,t_1,\cdots,t_n\}$ is a sequence of partitions of $[0,t]$ with mesh going to zero, then the Itô integral of $\sigma_t$ with respect to $W_t$ up to time t is a random variable

$$X_t=\int_{0}^{t}\sigma(s)dW_s=\lim_{n\to\infty}\,\sum_{i=1}^{n}\sigma(t_{i-1})(W(t_i)-W(t_{i-1}))$$

since $\sigma(s)$ is deterministic process and $W({t_i})-W(t_{i-1})\sim\mathcal{N}(0,t_i-t_{i-1})$ , thus $X_t$ is normally distributed such that

\begin{align*}

\mathbb{E}[X_t]&=\mathbb{E}\left[\lim_{n\to\infty}\sum_{i=1}^{n}\sigma(t_{i-1})(W_{t_i}-W_{t_{i-1}})\right]\\

&=\lim_{n\to\infty}\mathbb{E}\left[\sum_{i=1}^{n}\sigma(t_{i-1})(W_{t_i}-W_{t_{i-1}})\right]\\

&=\lim_{n\to\infty}\sum_{i=1}^{n}\mathbb{E}\left[\sigma(t_{i-1})(W_{t_i}-W_{t_{i-1}})\right]\\

&=\lim_{n\to\infty}\sum_{i=1}^{n}\sigma(t_{i-1})\mathbb{E}\left[W_{t_i}-W_{t_{i-1}}\right]\\

&=0 .

\end{align*}

By application of Ito's isometry formula, we have

$$\text{Var}(X_t)=\text{Var}\left(\int_{0}^{t}\sigma(s)dW_s\right)=\mathbb{E}\left[\left(\int_{0}^{t}\sigma(s)dW_s\right)^2\right]=\mathbb{E}\left[\int_{0}^{t}\sigma^2_sds\right]=\int_{0}^{t}\sigma^2_sds$$

Proof

If $Y(t)$ be a regular adapted process such that $\int_{0}^{t}\mathbb{E}\left[ Y^2(s)\right]ds < \infty$ then

$$\mathbb{E}\left[\int_{0}^{t}Y(s)dW_s\right]=0$$

Set $Y(s)=\sigma(s) e^{iuX(s)} $, we have

$$\int_{0}^{t}\mathbb{E}\left[ Y^2(s)\right]ds=\int_{0}^{t}\mathbb{E}\left[ \sigma^2(s) e^{2iuX(s)}\right]ds=\int_{0}^{t}\sigma^2(s)\mathbb{E} \left[ e^{2iuX(s)}\right]ds\tag 1$$

$X(t)$ is normally distributed with zero mean and a variance given by

$$\text{Var}(X_s)=\int_{0}^{s}\sigma^2(v)dv$$

thus

$$\mathbb{E} \left[ e^{2iuX(s)}\right]=\exp\left(2\text{i}\,u\,\mathbb{E}[X_s]-2u^2\text{Var}(X_s)\right)\tag 2$$

As a result

$$\int_{0}^{t}\mathbb{E}\left[ Y^2(s)\right]ds=\int_{0}^{t}\sigma^2(s)\exp\left(-2u^2\int_{0}^{s}\sigma^2(v)dv\right)ds<\infty$$