I think there are many approaches to setting risk tolerance/appetite limits. Here are some examples that you may find interesting (from the most clearest):

The Investment Risk Appetite of the Fund is:

- Relative (1 year) - Fund return 3 standard deviations from Reference

Portfolio (> -6.5% or > 8.5%);

- Absolute (1 year) - Loss greater than

25% of Fund value;

- Absolute (since inception) - Return >3% below

risk free rate;

Also read their Investment Beliefs.

This assumption of the Government’s risk appetite, referred to as the

“Risk Appetite Assumption”, is determined by reviewing, through

assetliability studies, the pension funding risk resulting from simply

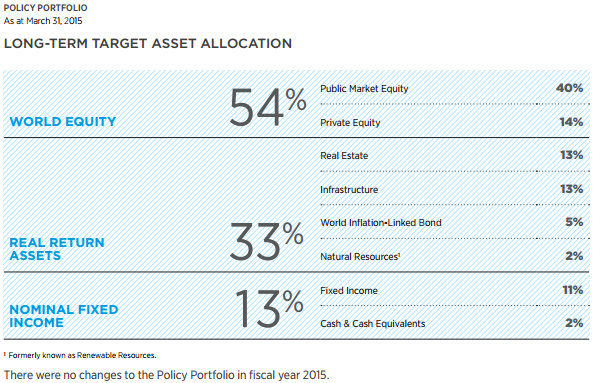

investing in a passive portfolio (aka Policy Portfolio) that would

replicate market indices of public debt and equity markets. This

passive portfolio is designed with the lowest possible investment risk

consistent with the Return Objective.

And going through their 2015 Annual Report I found this:

Active management activities form the second pillar of

PSP Investments’ approach. These activities are implemented within

an active risk limit and the risk appetite to generate additional

returns over the Policy Portfolio.

So my guess here is that they are creating their in-house index of Policy Portfolio and setting tracking error limits for their active funds.

You may be able to find some other approaches, but many pension funds seem to be less clear about their methodology. For example, see this presentation to get some idea about NBIM's approach. They also use Benchmark Portfolio and I think have tracking error limits along with other metrics.