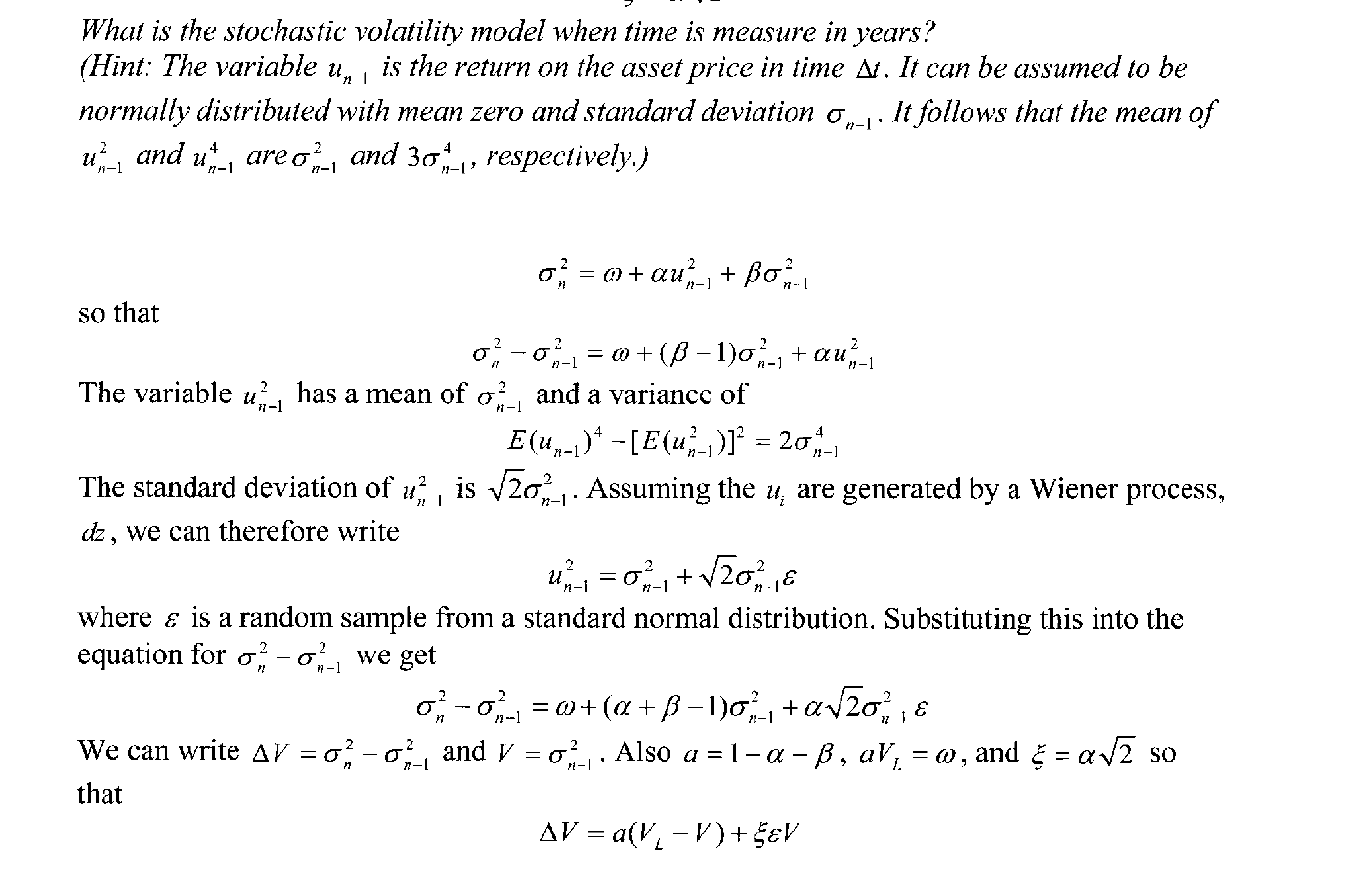

Here is the proof that the limit of GARCH(1,1)

$$\sigma_n^2 = \gamma V_L + \alpha u_{n-1}^2 + \beta\sigma_{n-1}^2$$

is equivalent to stochastic process of variance

$$d V = \alpha(V_L - V) dt + \xi VdW.$$

We have already assumed return $u_{n-1}$ is $(0,\sigma_{n-1}^2)$-normal, then $u^2_{n-1}$ can't be normal. But author said that

$$u^2_{n-1} = \sigma_{n-1}^2 + \sqrt{2}\sigma_{n-1}^2\varepsilon$$

where $\varepsilon$ is a random sample from a standard normal?

$\begingroup$

$\endgroup$

3

Options, Futures and Other Derivatives Solutions Manual Eighth Editionpage 171 Problem 22.14$\endgroup$