I also got a bit confused about understanding intuitively what happens in the limit with the Black-Scholes Call and Put values as the volatility goes to infinity, but after analyzing the derivation of the formula it becomes clear.

My confusion was about why the contribution of the $-K$ term disappear in the limit.

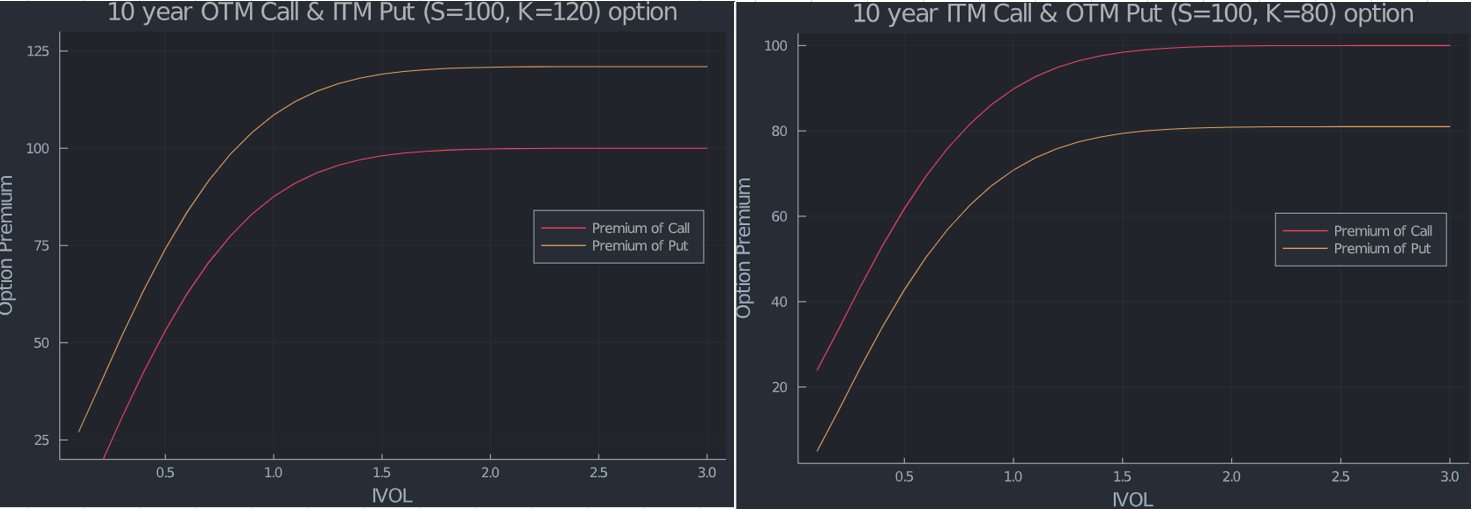

My faulty reasoning was a bit like this : If $S_T$ in the limit when $\sigma \to \infty$ is supposed to be big most of the time then I felt the option values should be $e^{-rT}(S_0 \cdot e^{rT} - K)$, the discounted payoff of the forward value. And if $S_T$ would be small most of the time, the limit would be $0$. This is wrong.

As LocalVol points out in the comments above, it is important to make a distinction between the size of the underlying and the probability that it has a certain size.

The price of the call is (using the risk neutral measure as usual and ignoring the initial discount factor)

$$

C = E[Max[(S_T - K, 0)] = E[S_T \cdot 1_{S_T \geq K} ] - E[K \cdot 1_{S_T \geq K}],

$$

where we have used indicator functions for the event that we end up in the money.

Let us look at the second term first. This is just

$$-E[K \cdot 1_{S_T \geq K} ] = -K \cdot \mathbb{P}(S_T \geq K).$$

That is, the value of $-K$ times the risk neutral probablility that this cash flow will occur. I will not rewrite all the math here, but we get that

$$

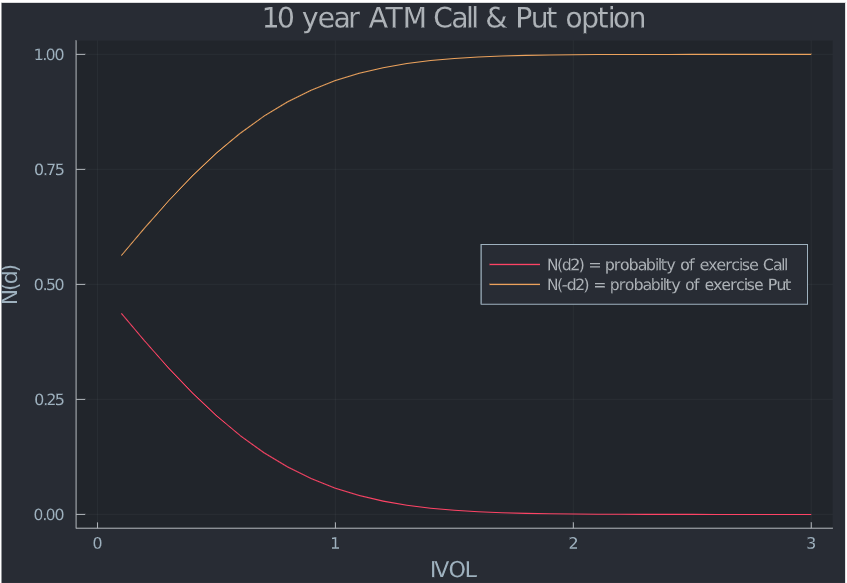

\lim_{\sigma \to \infty} \mathbb{P}(S_T \geq K) = 0.

$$

The probablity that we end up in the money goes to zero and the value of this second term goes to zero in the limit. If we were sampling the values of $S_T$, we would find that a larger proportion of paths goes down below K when $\sigma$ grows.

However, the point here is, as LocalVol points out, that although the probability of ending up in the money goes to zero, a larger and larger proportion of the expected value of $S_T$ comes from that region.

Mathematically we have

$$

\begin{eqnarray*}

\lim_{\sigma \to \infty} E[S_T \cdot 1_{S_T \geq K} ] &=& S_0 \cdot e^{rT} = E[S_T].\\

\lim_{\sigma \to \infty} E[S_T \cdot 1_{S_T < K} ] &=& 0.

\end{eqnarray*}

$$

More and more contribution of the expected value come from values of $S_T$ when $S_T \geq K$ as $\sigma$ grows, although the probability for those values to occur goes to zero.

So we have a sort of competition of limits here where the values of $S_T$ above $K$ increases faster than their probability to occur goes to zero, so to speak