- An excess return is the payoff of a zero cost portfolio. For example:

- $R_i - R_f$ is an excess return.

- $c \left( R_i - R_f \right) $ is an excess return for any $c \in \mathbb{R}$,.

- More generally, $R_i - R_j$ is an excess return for any returns $R_i$ and $R_j$.

Excess returns are nice to work with because you cans simply scale them up or scale them down and they're still excess returns. Let's imagine excess return $R_i - R_f$ has a market beta of $\beta_i$.

$$ R_i - R_f = \alpha_i + \beta_i \left( R_m - R_f \right) + \epsilon_i $$

Then excess return $\frac{1}{\beta_i} (R_i - R_f)$ has a market beta of $1$.

$$\frac{1}{\beta_i} \left( R_i - R_f\right) = \frac{\alpha_i}{\beta_i} + \left( R_m - R_f \right) + \frac{\epsilon_i}{\beta_i} $$

Excess return $\frac{1}{\beta_i} (R_i - R_f) -\frac{1}{\beta_j} (R_j - R_f) $ will have a market beta of 0.

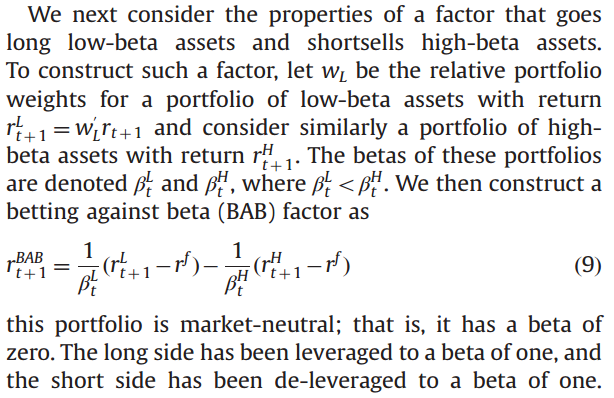

Since $\beta_H > 1$, multiplying by $\frac{1}{\beta_H}$ to obtain $\frac{1}{\beta_H} (R_H - R_f)$ is deleveraging the excess return $R_H - R_f$. Since $\beta_L < 1$, multiplying by $\frac{1}{\beta_L}$ to obtain $\frac{1}{\beta_L} (R_L - R_f)$ is leveraging the excess return $R_L - R_f$