General question: Are Sobol sequences any better than pseudo-random (PR) numbers (and thus still worth the effort) when the dimension is high? In most cases I'd say yes, if they are used with the Brownian Bridge (BB) path construction (or other effective dimensionality-reduction technique). Then again it depends on the type of option you are trying to price.

Have a look at these two pages that delve a little bit into this subject:

https://www.acenumerics.com/option-pricer-sobol-sequences.html

https://www.acenumerics.com/option-pricer-brownian-bridge.html

You can see there that for Asian options for example, Sobol numbers with BB give a huge advantage over PR numbers, even for high dimensions. For European barrier options the gain is smaller and for Bermudan/American options even less. But I still think that in all these cases you'll get better convergence wih Sobol & BB.

You can actually download the pricer from the site above and perform your particular test (American barrier with daily monitoring) so that you get the answer to your question, or at least a much better feel of what to expect. By the way, this will also point you to a different way of speeding up your MC pricing: Forgetting Matlab and going to C++ :)

By the way, this pricer does the American exercise with the Longstaff-Schwartz algo. How are you planning to do it?

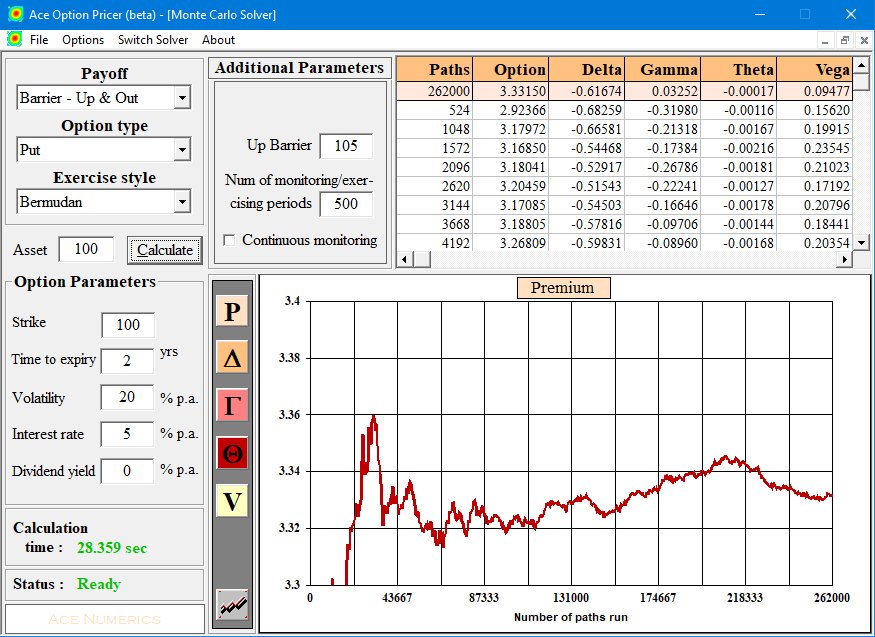

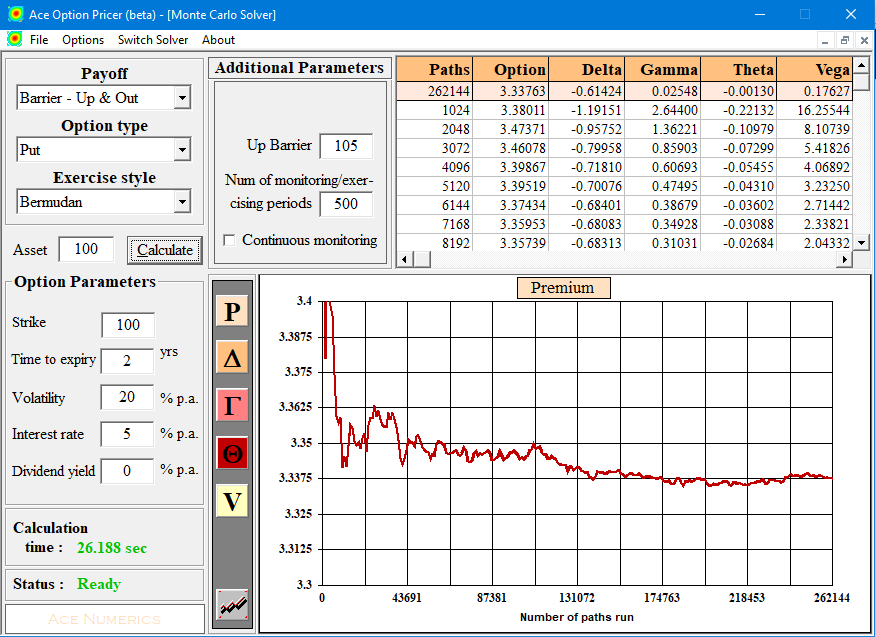

So I did a sample test for you, for an up and out Bermudan put with T=2Y and 500 monitoring points. First convergence graph is using PR numbers (what you call ordinary random numbers) with antithetics and the second is using Sobol sequences with BB path construction. For these I chose to use 10 basis functions (overkill, for accuracy) 65K paths for the L-S phase and 262K paths for the pricing.

A quick visual check gives the edge to Sobol & BB, though the gain is not dramatic. Unfortunately the pricer doesn't give you error estimates, so you have to go by the convergence graphs, which should give you an idea anyway. You can of course use the pricer yourself to do many more tests with different parameters and get a better idea of what to expect under different circumstances.

For Basket options I would expect the gains to be smaller. This is because the initial (better) dimensions of the Sobol variates will have to be allocated not only across the different time-points but also the different stocks in the basket. And if you use a stochastic volatility model then you'd also have the variance stochastic driver to take into account when deciding where to allocate your "best" Sobol dimensions.