Portfolio beta is a function of market vol, portfolio

vol and correlation between market and portfolio; so

correlation is indeed the only free variable. (But if you have complete control over the portfolio-construction process, you might as well target beta and then scale the weights so that you meet your volatility target.)

To control correlation,

you'll need a forecast of correlation first, and different setups

for getting these forecasts -- e.g. using historical

data with shrinkage, specific time horizons, etc -- may

give different results. What works well is an empirical question, but given that correlations are notoriously unstable, you should not expect to be able to fine-control correlation out-of-sample. In any case, eventually, these forecasts

are put into a correlation matrix (allowed assets + market).

If your portfolio was created via a optimization model, you may add

correlation directly, as a target or as a restriction.

Alternatively, you could create an overlay model, whose

aim is to maximize correlation subject to a restriction

on how much change to the portfolio you would be

willing to allow.

Update, following the comment: They way I suggest to handle

this is via a direct optimization of correlation. All

you then need is an optimization algorithm that is

capable of solving such models. Heuristics, for

instance, can handle such models (see Heuristic Optimisation in Financial Modelling or Heuristics for Portfolio Selection).

Whether a particular model make sense empirically is a, well,

empirical question; but the computation is quite straightforward. Let me sketch an example, using R, for the 'overlay' approach.

I'll keep this example very simple.

Suppose you have a

set R of return scenarios of your assets. Every

column hold the return of one asset. I also create a

'market' time-series, M. For simplicity, I use

historical data here. The data set consists of 48 industry portfolios provided by Kenneth French (I drop the other industry.)

library("NMOF") ## https://github.com/enricoschumann/NMOF

library("neighbours") ## https://github.com/enricoschumann/neighbours

R <- French("~/Downloads/French",

"49_Industry_Portfolios_daily_CSV.zip")

R <- R[seq(to = nrow(R), length.out = 500), 1:48]

R <- as.matrix(R)

M <- French("~/Downloads/French",

dataset = "market",

frequency = "daily")

all(row.names(R) %in% row.names(M)) ## check

## [1] TRUE

M <- M[row.names(R), ]

M <- as.matrix(M)

I create a random original portfolio. It is a zero-investment portfolio, with fairly large weights.

orig.portfolio <- runif(ncol(R), min = 0, max = 0.3)

orig.portfolio <- orig.portfolio - mean(orig.portfolio)

summary(orig.portfolio)

## Min. 1st Qu. Median Mean 3rd Qu. Max.

## -0.15474 -0.07257 0.02445 0.00000 0.06513 0.12166

round(sum(orig.portfolio), 8)

## [1] 0

The goal is now to create a zero-investment overlay, with maximum deviations of -0.025 to 0.025, say, that maximizes the correlation with the market M. The objective function cr is straightforward.

We later minimize, so I put a minus in front of the correlation.

cr <- function(x, orig.portfolio, R, M)

-c(cor(R %*% (x + orig.portfolio), M))

## cor(R %*% (orig.portfolio), M)

-cr(0, orig.portfolio, R, M)

## [1] 0.04762037

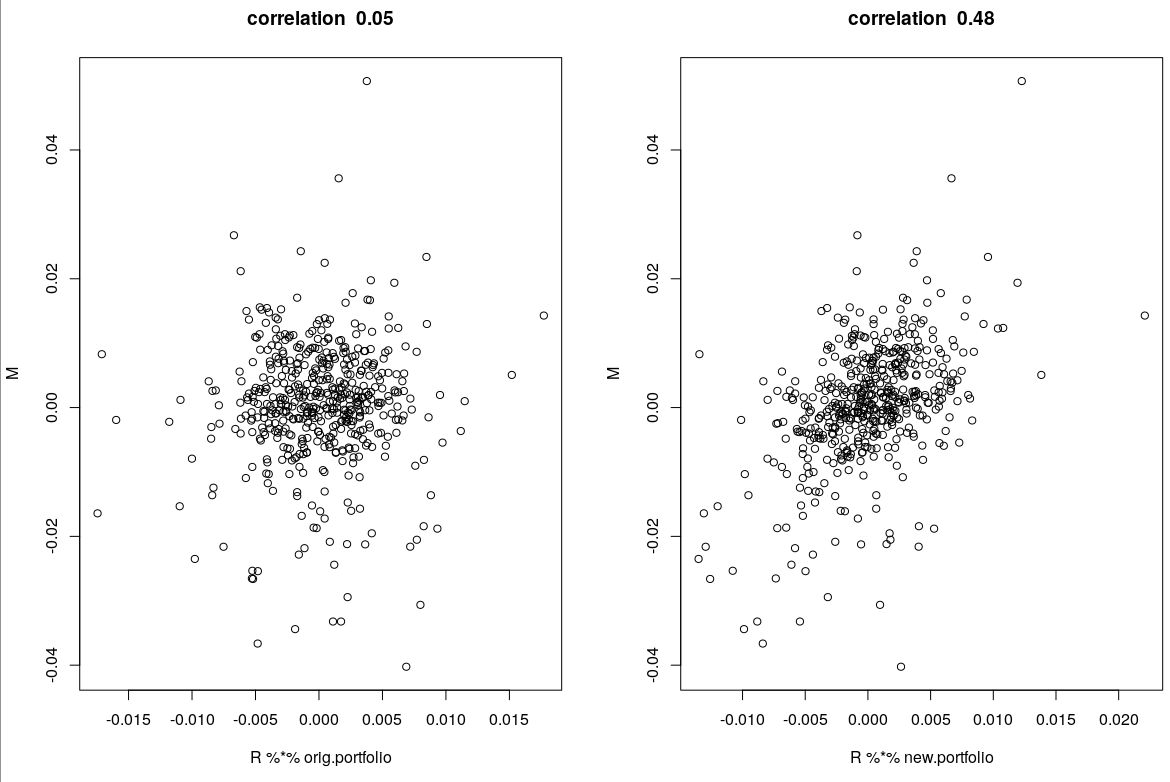

So the original portfolio had a correlation of 0.05. Now I minimize the function, using a method called Threshold Accepting.

nb <- neighbourfun(min = -0.025, max = 0.025, stepsize = 0.005)

sol <- TAopt(cr,

list(nI = 10000,

x0 = c(0.01,-0.01, rep(0, ncol(R)-2)),

neighbour = nb),

orig.portfolio = orig.portfolio,

M = M,

R = R)

-cr(sol$xbest, orig.portfolio, R, M)

## [1] 0.4776

So the new portfolio, which is still zero-investment, has a correlation of 0.48. For simplicity, I scale the new portfolio so that it has the same volatility as the original one. This will not affect the correlation.

new.portfolio <- orig.portfolio + sol$xbest

new.portfolio <- new.portfolio/sd(R %*% new.portfolio)*sd(R %*% orig.portfolio)

sd(R %*% orig.portfolio)

## [1] 0.004195

sd(R %*% new.portfolio)

## [1] 0.004195

-cr(new.portfolio-orig.portfolio, orig.portfolio, R, M)

## [1] 0.4776

We may also plot the portfolio returns under the scenarios R. On the left, the original portfolio; on the right, the portfolio with the overlay.

par(mfrow = c(1, 2))

plot(R %*% orig.portfolio, M,

main = paste("correlation ",

round(-cr(0, orig.portfolio, R, M), 2)))

plot(R %*% new.portfolio, M,

main = paste("correlation ",

round(-cr(new.portfolio-orig.portfolio, orig.portfolio, R, M), 2)))

(Disclosure: I am the maintainer of R packages used in the examples, and a coauthor of the papers I suggested above.)