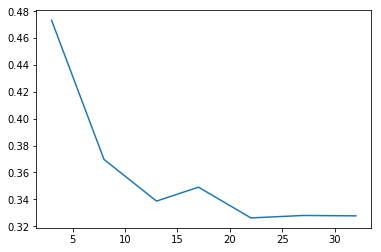

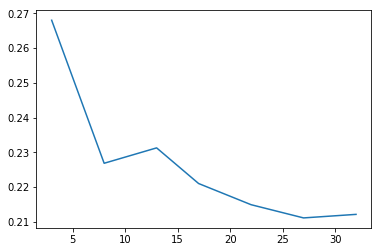

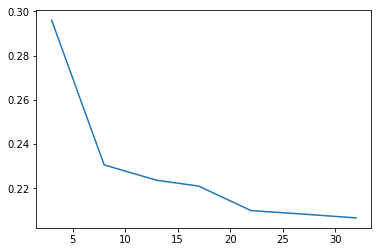

It's an empirical fact that the implied volatility of short term weekly options are significantly higher than options that expire in a few weeks, and the volatility of the near term options get even higher as we approach expiration. I've included some images of the ATM implied volatility of some option chains against days to expiration. What's the best way to model this behavior?