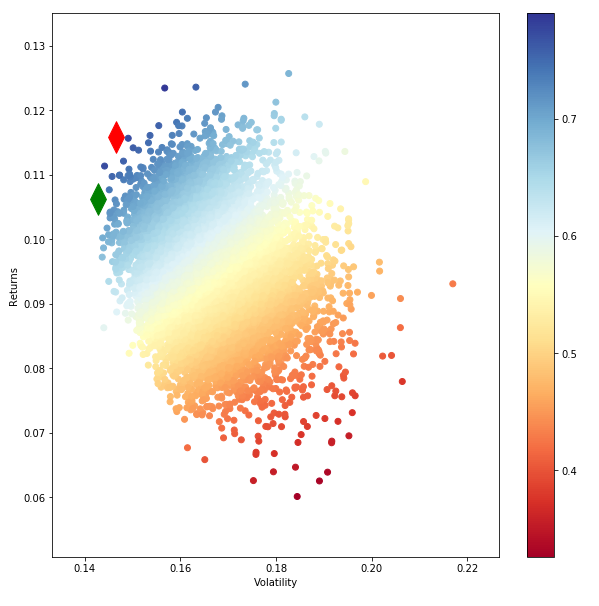

Hi I'm trying to draw an efficient frontier. Below is what I used. returns parameter consists of 9 column returns of portfolio. I selected 10,000 portfolios and this is how my efficient frontier looked like. This is not the usual frontier shape that is familiar to us.

Data set is 48_Industry_Portfolios_daily.csv, obtained from (http://mba.tuck.dartmouth.edu/pages/faculty/ken.french/data_library.html). The first 9 columns were selected

Can somone kindly explain me the issue.

def portfolio_annualised_performance(weights, mean_returns, cov_matrix):

returns = np.sum(mean_returns*weights ) *252

#print ('weights shape',weights.shape)

#print (' Returns ',returns)

std = np.sqrt(np.dot(weights.T, np.dot(cov_matrix, weights))) * np.sqrt(252)

#print ('Std ',std)

return std, returns

def random_portfolios(num_portfolios, mean_returns, cov_matrix, risk_free_rate):

results = np.zeros((3,num_portfolios))

weights_record = []

for i in range(num_portfolios):

weights = np.random.random(48)

weights /= np.sum(weights)

weights_record.append(weights)

portfolio_std_dev, portfolio_return = portfolio_annualised_performance(weights, mean_returns, cov_matrix)

results[0,i] = portfolio_std_dev

results[1,i] = portfolio_return

results[2,i] = (portfolio_return - risk_free_rate) / portfolio_std_dev

return results, weights_record

def monteCarlo_Simulation(returns):

#returns=returns.drop("Date")

returns=returns/100

stocks=list(returns)

stocks1=list(returns)

stocks1.insert(0,"ret")

stocks1.insert(1,"stdev")

stocks1.insert(2,"sharpe")

print (stocks)

#calculate mean daily return and covariance of daily returns

mean_daily_returns = returns.mean()

#print (mean_daily_returns)

cov_matrix = returns.cov()

#set number of runs of random portfolio weights

num_portfolios = 10000

#set up array to hold results

#We have increased the size of the array to hold the weight values for each stock

results = np.zeros((4+len(stocks)-1,num_portfolios))

for i in range(num_portfolios):

#select random weights for portfolio holdings

weights = np.array(np.random.random(len(stocks)))

#rebalance weights to sum to 1

weights /= np.sum(weights)

#calculate portfolio return and volatility

portfolio_return = np.sum(mean_daily_returns * weights) * 252

portfolio_std_dev = np.sqrt(np.dot(weights.T,np.dot(cov_matrix, weights))) * np.sqrt(252)

#store results in results array

results[0,i] = portfolio_return

results[1,i] = portfolio_std_dev

#store Sharpe Ratio (return / volatility) - risk free rate element excluded for simplicity

results[2,i] = results[0,i] / results[1,i]

#iterate through the weight vector and add data to results array

for j in range(len(weights)):

results[j+3,i] = weights[j]

print (results.T.shape)

#convert results array to Pandas DataFrame

results_frame = pd.DataFrame(results.T,columns=stocks1)

#locate position of portfolio with highest Sharpe Ratio

max_sharpe_port = results_frame.iloc[results_frame['sharpe'].idxmax()]

#locate positon of portfolio with minimum standard deviation

min_vol_port = results_frame.iloc[results_frame['stdev'].idxmin()]

#create scatter plot coloured by Sharpe Ratio

plt.figure(figsize=(10,10))

plt.scatter(results_frame.stdev,results_frame.ret,c=results_frame.sharpe,cmap='RdYlBu')

plt.xlabel('Volatility')

plt.ylabel('Returns')

plt.colorbar()

#plot red star to highlight position of portfolio with highest Sharpe Ratio

plt.scatter(max_sharpe_port[1],max_sharpe_port[0],marker=(2,1,0),color='r',s=1000)

#plot green star to highlight position of minimum variance portfolio

plt.scatter(min_vol_port[1],min_vol_port[0],marker=(2,1,0),color='g',s=1000)

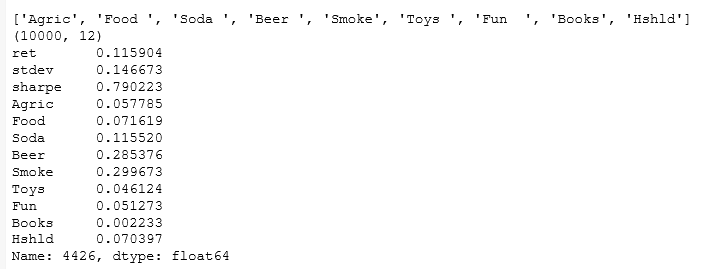

print(max_sharpe_port)

updated answer

Also I'm asked to compare portfolio variance using different regularizes and to use a validation methods to find the optimal parameters. Can we use python to do this?