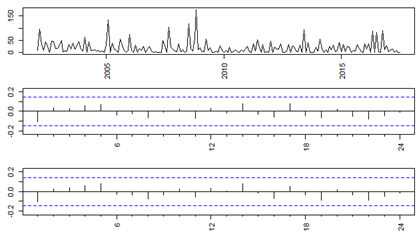

I have an ARIMA model for monthly returns of the brazilian stock market index. Then I test the residuals of the model for ARCH effects. The ACF/PACF of squared residuals show that there are no significant autocorrelations. Portmanteu and McLeod-Li tests also show that there are no heteroscedasticity. Nevertheless, Lagrange Multipler test appear to show there is heteroscedasticity for lags 1 to 8 and the plot of squared residuals itself look a little bit like there might be some volatility clustering. When I fit GARCH models (GARCH, gjrGARCH, AVGarch, TGARCH...), the ones with smallest BIC are (0,1) models, for which the beta is very close to 1 and so the conditional sd forecasts decrease very slowly. This appears to be caused by the fact that no GARCH model should be used, is that correct?

Below: the squared residuals plot, ACF and PACF of squared residuals.