In Basel/CRR (capital requirement regulation) there are various approaches for the estimation of capital requirements.

For corporate exposures there is the Foundations IRB approach (F-IRBA, own estimates of PD) and the Advanced IRBA (A-IRBA) with own estimates of loss-given-default and conversion factors. For the exposures to specialised lending (e.g. project finance) a so called slotting approach exists in addition.

These approaches have increasing demands for model sophistication and especially data availability. The approaches used for capital calculations are reported in the disclosure reports for each bank.

my question: are such numbers available in an aggregate basis somewhere?

I would be interested in questions like "What is the share of Corporate exposure in F-IRBA at European banks as opposed to Standardized Approach and A-IRBA?".

Is such data collected and made available somewhere?

PS: I am aware that such questions are not 100% on-topic for a quant site but I made the experience that quants should know how the peer group looks.

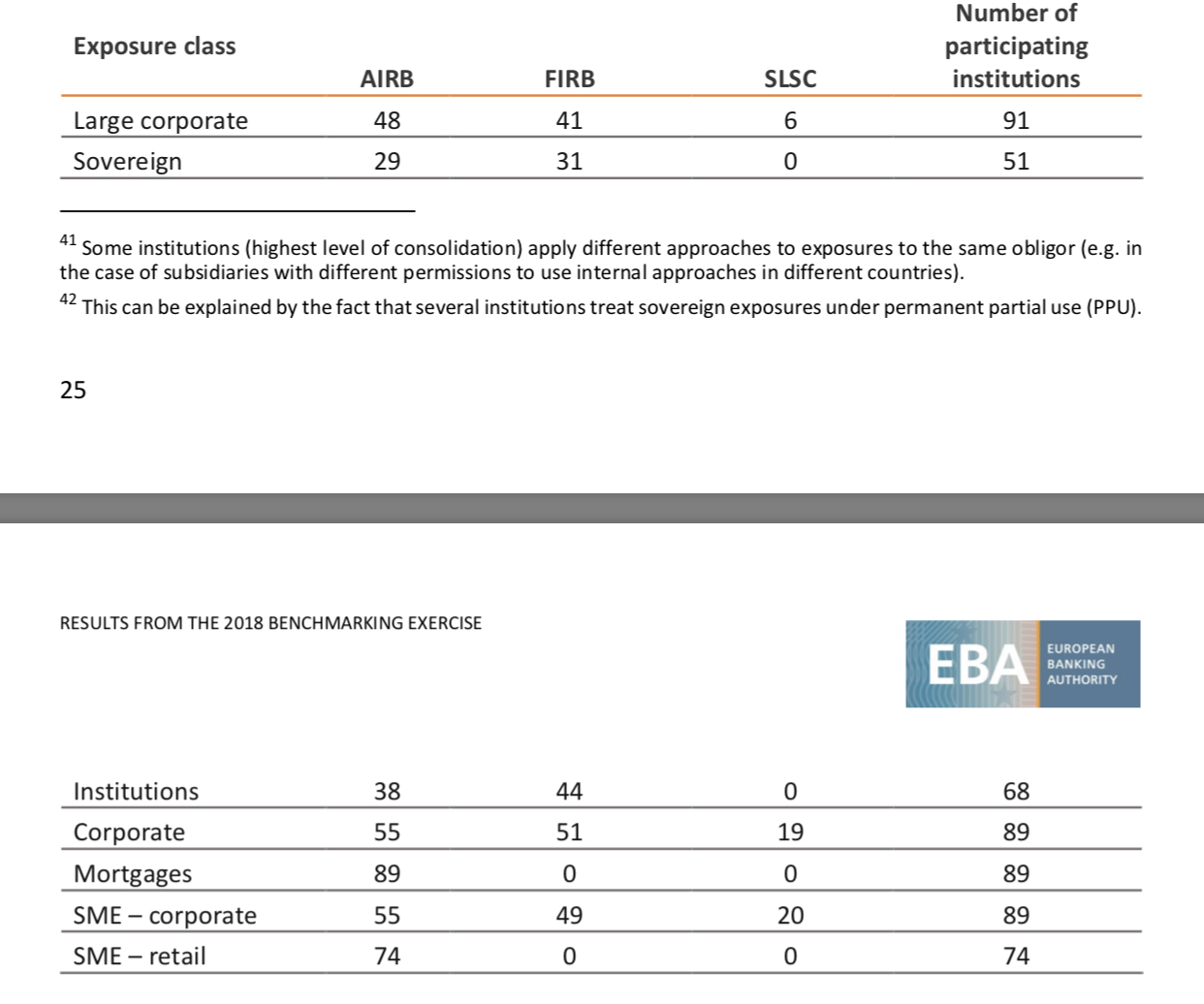

Table 13answers your question eba.europa.eu/documents/10180/1720738/… $\endgroup$