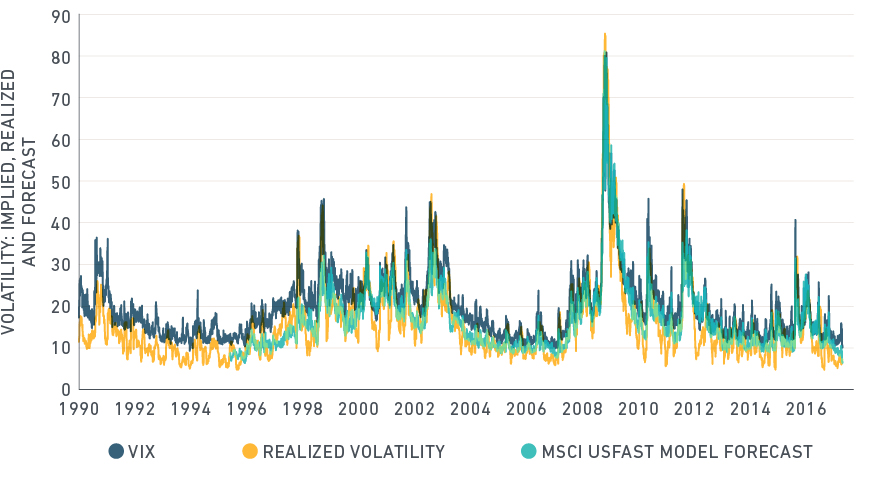

The VRP is usually displayed by charts like this one:

It's easy to see that, for most of the time, options are priced by using volatility which will reveal itself larger than the realized one. So VRP is simply the arithmetic difference between implied (or model-free) volatility and realized volatility.

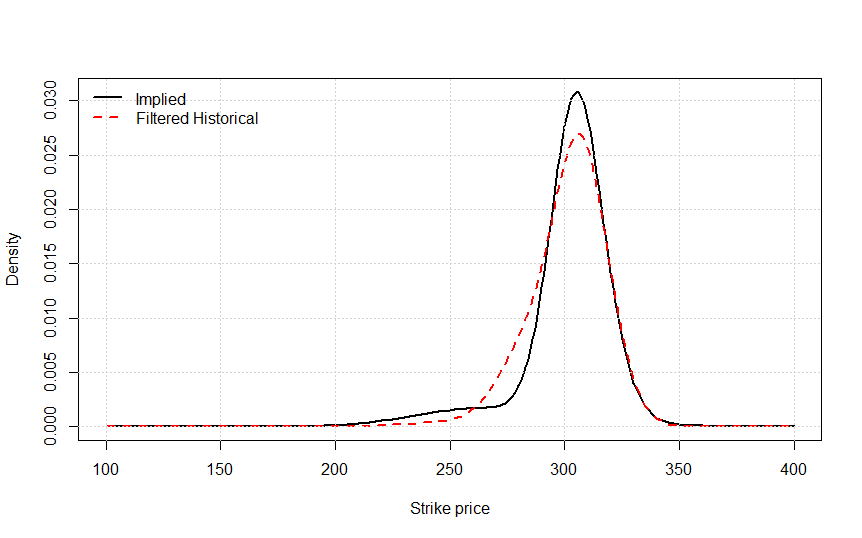

However, I'm wondering what's the best way to measure and quantify VRP when we have density functions instead of volatility measures. In the following case, for example, we have two arrays with probability densities and an array with strike prices:

How would you quantify the VRP?