Taleb makes the claim in this paper (and others) that there exists some sort of bound on the variance of a binary forecast such that if a forecaster's binary predictions exceed the bounds on variance there exists a method to arbitrage him. Would someone familiar with the dispute (and perhaps various other papers) be able to explain exactly and technically what he means?

$\begingroup$

$\endgroup$

4

-

5$\begingroup$ Can you provide a link? I think I know what the discussion is about, but without a link, I may be making assumptions regarding the discussion. $\endgroup$– Dave HarrisCommented Aug 9, 2019 at 22:34

-

$\begingroup$ Is it about this issue? $\endgroup$– RaskolnikovCommented Aug 10, 2019 at 22:09

-

$\begingroup$ Yes. I think his main point revolves around the volatility of Silver's forecasts being too high. He claims that this would expose Silver to arbitrage if he were to trade on his forecasts. I do not understand how he can know this. Is there a rigorous proof or is it just Taleb's "feeling" that the vol of Silver's forecast is too high. $\endgroup$– rozCommented Aug 11, 2019 at 2:29

-

$\begingroup$ I just want to note that if you replace volatility with entropy, I believe Taleb's argument is correct (you end up with a uniform distribution). $\endgroup$– justaskingCommented Nov 14, 2023 at 10:38

Add a comment

|

2 Answers

$\begingroup$

$\endgroup$

6

hope I am not too late to the party.

tl;dr Taleb's paper draws incorrect conclusions from a set of wrong assumptions. In practice, the movements of the forecast at 538 are very much in line with what can be defined an "arbitrage free prediction" based on a binary option model.

The gist of the article is summarized in its incipit.

A standard result in quantitative finance is that when the volatility of the underlying security increases, arbitrage pressures push the corresponding binary option to trade closer to 50%, and become less variable over the remaining time to expiration. Counterintuitively, the higher the uncertainty of the underlying security, the lower the volatility of the binary option. This effect should hold in all domains where a binary price is produced – yet we observe severe violations of these principles in many areas where binary forecasts are made, in particular those concerning the U.S. presidential election of 2016.

There are quite a number of fallacies in the above statements:

Taleb's assumptions:

- Any forecast of a dichotomous outcome is equivalent to the pricing of a binary option.

- Increase in the underlying's volatility pushes a binary option price to trade close to 50% of its payoff. Incorrect

- Increase in the underlying's volatility reduces the volatility of the option price itself. Incorrect

Taleb's Conclusions:

Any forecasts of binary outcomes should behave according to principles 1 and 2. Therefore any prediction that - at the same time - a) claims high uncertainty and that b) fluctuates heavily, goes against no-arbitrage principle, or put otherwise: 538's predictions is rubbish. For the sake of clarity, this is not a valid claim!

Analysis of assumption no.1

Assume we are happy with 1, i.e. we agree to model the an election forecast as a binary option. From a financial perspective, the underlying S can be interpreted as the "consensus" for the two candidates, being the strike K the amount of consensus required to "exercise" the option (i.e. to claim the elections). Tbh, one could argue on the appropriateness of the choice of a binary option since the "consensus variable" S that has a lower bound (zero, as prices cannot go negative). Let us pass on that critique assuming that it is not a big issue when S and K are sufficiently distant from 0. Side note - we will be working with an European Call Option (as elections are normally "callable" only at expiry, i.e. only after election day has passed - wink wink).

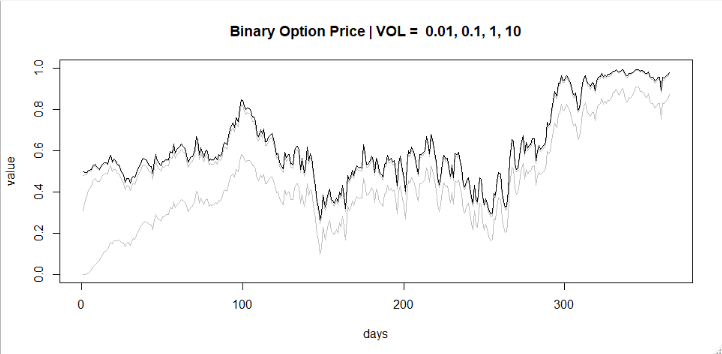

Analysis of assumption no.2 We hereby simulate how the price of a binary option with the above mentioned features behaves with changes in volatility. We examine the outcome for ATM, ITM, and OTM options, for the sake of completeness. Regardless from the moneyness of the option, the increase in volatility pushes the option value towards 0. This invalidates assumption no.2

The price of an OTM binary option is 0% of the payoff for very small and for very large volatilities. There is a sweet volatility spot where option value is maximized, which can be interpreted as the level of volatility that maximises the chances of S > K at maturity. Away from that sweep spot the increasing chances that the S < K at maturity push option value to 0.

The price of an ATM binary option is exactly 50% of its payoff for small volatilities then decays to 0. The higher the volatility the higher the chances that the S < K at maturity.

The price of an ITM binary option is 100% of the payoff for small volatilities then decays to 0. The higher the volatility the higher the chances that the S < K at maturity.

A more extensive discussion on binary option vega can be found here: How does volatility affect the price of binary options?

Analysis of assumption no.3

We hereby simulate how the price of a binary option fluctuates as it approaches maturity, based on the volatility of the underlying process S. We examine here the case of an ATM Option, outcome for OTM and ITM are however aligned. Simulation covers one year time period prior to the exercise. Our methodology requires that the same binary option is re-priced daily based on a) the TTM (time-to-maturity) and on b) the value of the underlying discrete random process S which is assumed to behave as a random walk. Perfect knowledge of the underlying process is assumed, i.e. the vol of the binary option is perfectly aligned to the true volatility volatility of S.

The increase in volatility pushes the option value towards 0 for larger TTM but the process converges (i.e the forecast) converges closer to expiry. Regardless from the volatility of the underlying process, the price of the binary option never converges to 50% This invalidates assumption no.3

There is an interesting post on Quora that highlights how Taleb "proves" his point by means of a chart (Fig 3. in Taleb's paper) generated with a incorrect Mathematica code. I am not sure if he purposefully uses that chart to deceive a reader already confused by his math or if this is a genuine - though misguided - attempt of his to numerically prove the theory. Either way, it is not correct.

I feel there is quite some confusion revolving this paper and its commentaries, partially due to the cryptic and unapologetic style of Taleb as well as to the fact that many opinions on the issue are imo excessively polarized by the pov of his follower/detractors.

For the sake of transparency: all the analysis above are based on the implementation of binary option pricer from https://www.quantlib.org/ and the script used for the analysis is available for scrutiny and corrections at my github.

-

$\begingroup$ That was quite a nice read on a Wednesday morning, thanks. $\endgroup$ Commented Nov 11, 2020 at 8:10

-

2$\begingroup$ How did you model $S$? If you used Geometric Brownian Motion, then with discretization, as volatility increases, there could be paths that are absorbed into 0 thus the result that all OTM/ATM/ITM prices converge to 0. However 0 should not be an absorbing level in this case. If GBM, it would be nice to have the same results but with Reflected Brownian Motion. $\endgroup$ Commented Nov 11, 2020 at 9:37

-

$\begingroup$ Upvoted -- this should (in my opinion) be the accepted answer. Very nicely done! $\endgroup$– Brian BCommented Nov 11, 2020 at 13:53

-

6$\begingroup$ Are you aware that Nassim Taleb does not model the forecast probability as a binary option price (with an underlying following GBM)? The decay of price as volatility increases you are showing is well understood. Taleb uses a Bachelier-type model where the underlying follows an arithmetic Brownian motion. In that case rather than $N(d_2) \to 0$ as $\sigma \to \infty$ we have $N\left( \frac{S_0-K}{\sigma \sqrt{T}}\right) \to 0.5$. I assume zero drift here to illustrate. $\endgroup$– RRLCommented Nov 14, 2020 at 20:25

-

4$\begingroup$ If you are going to criticize Taleb in a public forum, make sure to have all your ducks in a row. I would also highly recommend against casting aspersions by insinuating that a paper which acknowledges Bruno Dupire, Peter Carr, et al. is propagating "fallacies" and that Taleb is either "misguided" or intentionally trying to "deceive a reader." -- incorrect analysis by you here notwithstanding. $\endgroup$– RRLCommented Nov 14, 2020 at 23:26

$\begingroup$

$\endgroup$

$\endgroup$

3

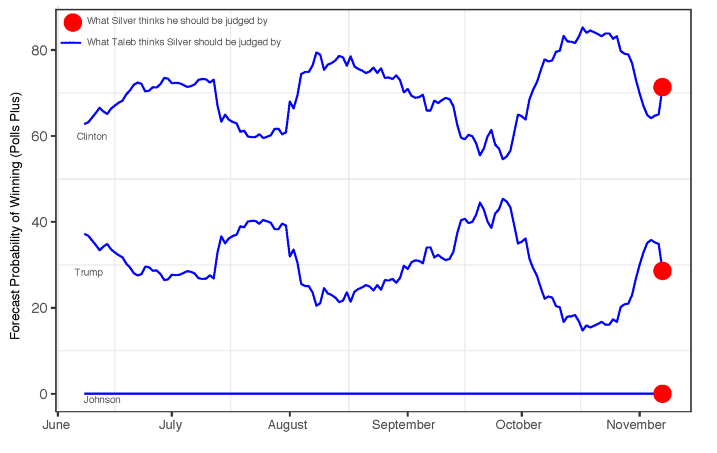

Taleb argues that under uncertainty, election forecasts should be seen as a Binary option. A similar thought is presented by De Finetti's principle that probability should be treated like a two-way "choice" price. Therefore, under high levels of volatility, forecast should not have extreme variation across time (equivalently, the price of the binary option should not change significantly even if polls reveal a large change in the dynamics among candidates). Under high levels of uncertainty, the price of the binary option converges to 0.5. Therefore, the probability of winning the elections in a two-candidate environment should converge to 0.50. A quick look on Silver's forecasts, shows high volatility across time. For instance, Trump's probability of winning the elections ranges roughly from 0.15 to 0.45

For more details on Taleb's no-arbitrage argument, one should check his recent publication and a response to this publication:

Taleb, Nassim Nicholas. "Election predictions as martingales: an arbitrage approach." Quantitative Finance 18.1 (2018): 1-5.

https://www.tandfonline.com/doi/citedby/10.1080/14697688.2019.1639802?scroll=top&needAccess=true

answered Aug 12, 2019 at 10:03

-

$\begingroup$ I understand that as volatility increases the price of the binary approaches 0.5. I also understand the mapping between binary bets, choice prices, and probabilities. What I do not understand is what exactly the arbitrage process is. Taleb makes a claim that Silver can be arbitraged via a Dutch book sort of procedure. But I do not see how. I have read the papers you linked and either they do not explain it or I am just not understanding it. Do you know how? $\endgroup$– rozCommented Aug 12, 2019 at 13:34

-

$\begingroup$ Buying the binary when its price is very low and selling it when its price is very high based on the assumption that vol is very high is not an arbitrage; you are just trading vol. So if this is the process that Taleb is referring to when he says arbitrage, I think he is not correct. $\endgroup$– rozCommented Aug 12, 2019 at 13:38

-

$\begingroup$ @roz The key point is that the prices should reflect proper updating, which Taleb defines as martingale valuation-based revision. Otherwise, the pricing is systematically wrong and theoretically can be exploited by Dutch booking. e.g. one casual commentator suggests that when the 538 forecast for a candidate goes up one day, it is more likely to go up the next day as well. Clearly the "underlying volatility of the asset" (as Taleb would say) is not being properly priced in at any stage. $\endgroup$ Commented Jan 14, 2021 at 22:40