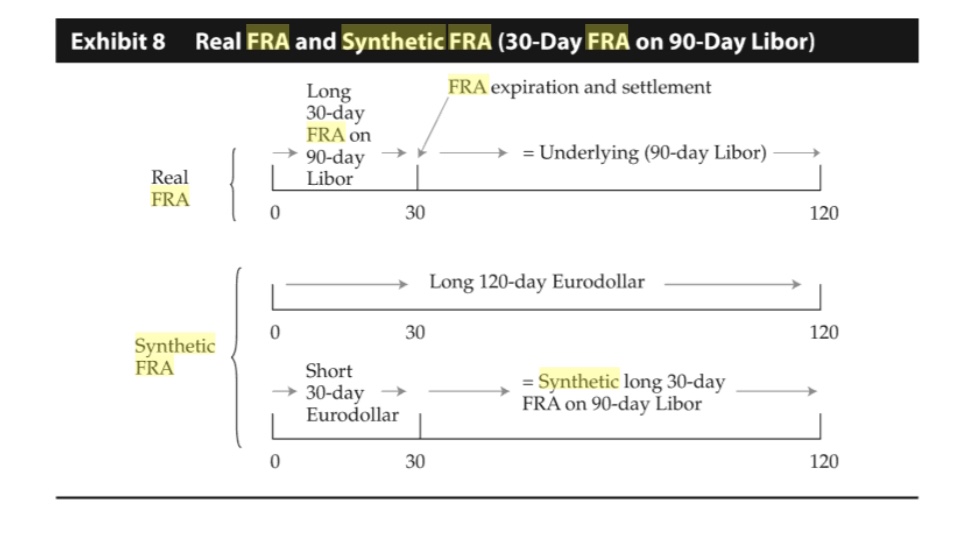

In order to create a synthetic FRA position of 30-day FRA on 90-day LIBOR, the diagram below shows that we can enter into positions by going long a 120-day Eurodollar contract and short a 30-day Eurodollar contract.

Here is a section from Basic of Derivative Pricing and Valuation, Reading 57, a part of CFA curriculum 2019 Level 1

Q: Looking at the diagram, is my understanding correct that what the diagram showing is 30 days from now we have to close the long position of 120-day Eurodollar at T=30 in order to achieve no exposure over 30-day period?