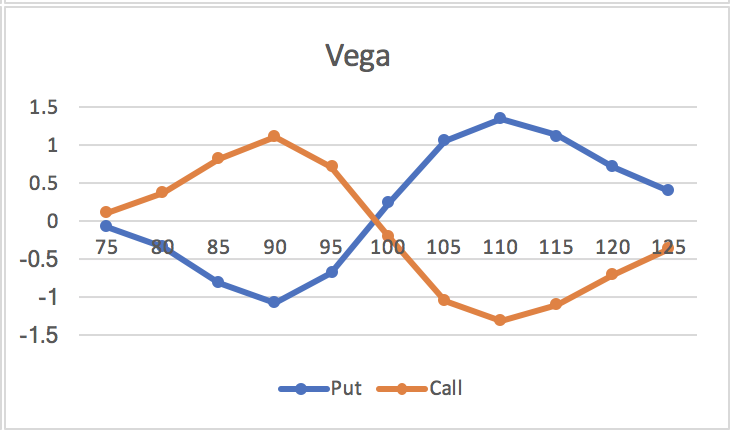

I'm calculating the greeks for a hypothetical binary option, and I'm getting a symmetrical parabola for the vega's of both put and call options that are OTM, ATM, and ITM. Both of them dip into negative territory however. The vega for the call becomes negative when the binary option moves more into-the-money, while the inverse happens for my put.

I read that calls and puts always have positive vegas, which is why I'm confused about my graphed results (see picture; x-axis represents different spot prices, all else equal). Can anyone shed light into this?