I'm reading about the Hull-White model, I understand the math behind it and logic but what I am struggling to understand is how it's actually used in practice ? How can we combine it with technics like Monte-Carlo for IRD options pricing ? Can someone simplify this from a practitioner point of view with some example please ? thank you

$\begingroup$

$\endgroup$

Add a comment

|

2 Answers

$\begingroup$

$\endgroup$

4

The Hull-White model is an no-arbitrage short rate model. It is used to price interest rate derivatives such as caps and floors. It generalises the seminal equilibrium model from Vasicek (1977).

The Model

The model postulates that $$\mathrm{d}r_t=\kappa_t(\theta_t-r_t)\mathrm{d}t+\sigma_t \mathrm{d}W_t.$$ Two of the key model features are that

- the short rate $r_t$ is mean-reverting (if rates are far away from the long-term mean $\theta$, they will likely converge back to this level, $\kappa_t$ corresponds to the speed of mean reversion)

- the short rate $r_t$ is normally distributed (negative interest rates are thus possible. This was long seen as a downside but can be useful nowadays).

The model is very tractable and allows for closed-form pricing formulae of zero-coupon bond, bond options (thus caps and floors) and swaptions. Calibration is thus very easy.

The model belongs to the class of affine term-structure models allowing you to write the price of a zero-coupon bond as $P(t,T)=\exp\left(A(t,T)+r_tB(t,T)\right)$. The Cox-Ingersoll-Ross (1985) model also belongs to this class.

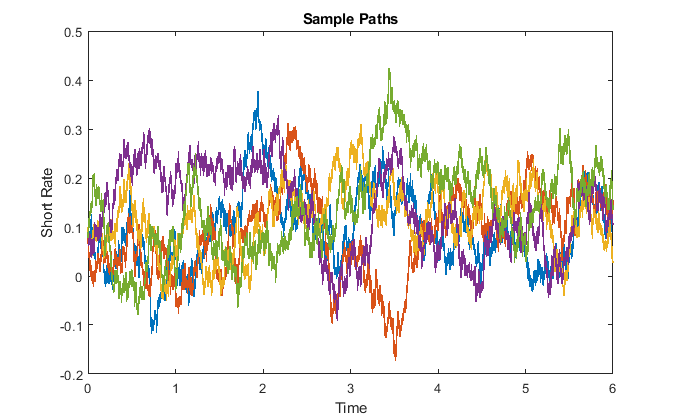

Because the model assumes a normal distribution, Monte Carlo simulations are also very simple to implement. You can use a simple Euler approximation to simulate different paths: $$r_{t+\Delta t}=r_t+\kappa_t(\theta_t-r_t)\Delta t+\sigma_t \sqrt{\Delta t}Z,$$ where $Z\sim N(0,1)$.

Let $\kappa_t\equiv2$, $\theta_t\equiv0.1$ and $\sigma_t\equiv0.2$. Here are some realisations

One downside is that the volatility is not state-dependent. You'd expect a high short rate to more volatile than a short rate close to zero. The model assumes a constant (or at least deterministic) instantaneous variance. The CIR model is a better choice in this respect.

Just as a note, let $R(t,T)$ be the spot interest rate. Then, $\mathbb{C}\text{orr}(R(t,T),R(t,S))=1$ for all $T,S$, i.e. a shifting a single bond yield will cause a parallel shift to the entire yield curve. That's not quite true in real life data but an implication of the model.

Pricing

From the fundamental theorem of asset pricing, we obtain $$P(t,T) = \mathbb{E}^\mathbb{Q}\left[\exp\left(-\int_t^T r_s\mathrm{d}s\right)\bigg|\mathcal{F}_t\right].$$ You can thus price bonds by knowing the short rate. Regarding bond options, you can write down a PDE similar to the Black-Scholes PDE and solve it easily in closed-form: $$P_t+\mu(t,r)P_r+\frac{1}{2}\sigma(t,r)^2P_{rr}-rP=0.$$ Caps and floors are just portfolio of zero-coupon bond options. This way, you can compute the prices of liquid, observable products and use them for calibration (minimise sum of squared relative errors). The result are the risk-neutral parameters for the short rate process.

Having found these values, you can price arbitrary complicated products, using Monte Carlo, finite differences or trees. The underlying logic for Monte Carlo simulations, simulating paths, computing payoffs, taking averages and discounting them still applies. Simple interest rate options, caplets and floorlets, can be priced in closed-form though.

You can find formulae about the distribution, bond price and bond option price on the wikipedia page. An excellent source on interest rate models is the book from Brigo and Mercurio. This book includes most (all?) relevant formulae.

-

$\begingroup$ I do not think it makes sense to use the Euler approximation. The mean and covariance can be calculated explicitly so this is not necessary. $\endgroup$– g gCommented Aug 15, 2020 at 7:25

-

$\begingroup$ @gg Yes it can and you're right. I highlighted in my answer that most simple products can indeed be priced using closed-form formulae. You don't need Euler to price a simple bond put option. That's one of the great advantages of the model. But 1) you may want to price path-dependent exotics and then Euler + MC is a valid approach and 2) OP explicitly asked about Monte Carlo simulations. $\endgroup$– KevinCommented Aug 15, 2020 at 9:55

-

1$\begingroup$ You misunderstood my comment (which was probably not very clear in the first place). It was not about using MC to value exotics but about the simulation of the short rate. Since you can solve the SDE explicitly you do not need to approximate the process by discretisation. Ultimately you only have to draw proper multivariate normals. This approach has the added advantage that you can include the exact (joint normal) distribution of the discount/bank account i.e. $Y(t)=\int_0^t r(\tau)d\,\tau$. $\endgroup$– g gCommented Aug 15, 2020 at 12:39

-

$\begingroup$ Yeah that’s also right, the SDE boils down to an OU process and you can easily solve for the short rate. For displaying a few sample paths, there’s no difference whether you use an Euler scheme or use the solution for $r_t$. Both are valid approaches which give you some illustrative sample paths. I only picked the Euler approach because it was simpler (shorter) to write down. I merely wanted to show how to get some graphs and not argue in favour of elegance or efficiency. But your suggestion is of course absolutely correct! $\endgroup$– KevinCommented Aug 15, 2020 at 12:41

$\begingroup$

$\endgroup$

The unembellished Hull-White model is not used very much in practice, because it is under-parameterized to handle a term structure of risk-free rates, and hence cannot be calibrated in any reasonable way.

As you have probably remarked, in its usual form it starts the short rate $r$ at some single value, and evolves $r$ according to just a couple volatility and drift parameters. This prevents it from fitting to more than three market instruments.

I have occasionally seen straight Hull-White used for pricing embedded bond options, in particular on Bloomberg terminals, but otherwise have not observed a professional employing it since the 1990s.

Now, if you embellish HW with full term structures of forward short rates, into what we call the 1-factor Generalized Vasicek or HJM model, you end up with a near-equivalent relatively parsimonious interest rate model suitable for simultaneously treating multiple interest rate products. (Be careful: if you get as exotic as Bermudan/American-exercise swaptions you must have 2 factors)

Once you calibrate the generalized model to market instruments, you can use it for pricing less liquid stuff. Alternatively, to use it for risk, you would fit it in subjective probability space using a Kalman Filter, as in this paper by Babbs and Nowman. I also refer you to these notes from an MIT class.

The Wikipedia page is not bad for HJM; I'll paraphrase:

Basically we take the term structure of zero-coupon bond prices as $P(t,T)$ and define forward rates $f$ by $P(t,T)=e^{-\int_t^T f(t,s) ds}$, where in practice you assume $f$ is some kind of step or piecewise polynomial function. No-arbitrage arguments end up controlling the drift in $f$ according to the volatility term structure.

If we assume volatility takes the simple form $\sigma(t,T) = \sqrt{(T-t) \bar{\sigma}^2}$ then the evolution equation is then more-or-less the same as Hull-White:

$$ df = k dt + \nu dW $$

where when we put in all the machinery, that expands to

$$ df(t,u) = \left( \sigma(t,u) \int_t^u \sigma(t,s)^{T} ds \right) dt + \sigma(t,u) dW_t $$