In his paper "Smile Dynamics IV" (https://www.fields.utoronto.ca/programs/scientific/09-10/finance/derivatives/bergomi.pdf) as well as in his book "Stochastic Volatility Modeling" (Chapter 9.10) Lorenzo Bergomi proposes a "Skew Arbitrage Strategy". As I understand his logic, he is saying that for short maturities the skew stickiness ratio should be close to 2 (i.e. the implied ATM vol move for an dS_rel % spot move is 2 * Skew * dS_rel ). However, empirically the realised absolute spot move tends to be less than that, so one could buy a gamma neutral 1 month 95/105 risk reversal, delta hedge and hold it for one day. Since we are gamma neutral, as given by a Taylor expansion this position's PnL should be determined by

skew PnL + Vega PnL + "Mark to Market PnL"

"skew PnL" is proportional to realised spot vol covariance minus implied spot vol variance and will on average be positive as the realised stickiness is smaller than the implied one.

Vega PnL is small compared to the rest and basically just adds some noise.

"Mark to Market PnL" comes from recalibrating the vol model. More precisely, he is using a simple vol model, which is quadratic in log moneyness

$$\widehat{\sigma}(x)=\sigma_{0}\left(1+\alpha\left(\sigma_{0}\right) x+\frac{\beta\left(\sigma_{0}\right)}{2} x^{2}\right)$$

So each day, we would have to recalibrate the skew and curvature. In his book and paper Bergomi says that this Mark to Market PnL should be negligible. However, if I buy a 30 day option today, this will be a 29 day option tomorrow. The 95/105 skew decays (i.e. becomes more negative) as time to maturity goes down, so there should be a downward drift on the PnL. I tried to replicate the strategy and can indeed observe such a downward drift. It is smaller than the skew PnL, but has a non negligible effect on the PnL. In my replication I am using the S&P and my time period is 2010 to 2019, while Bergomi is using Eurostoxx and 2002-2010, so it is possible that I am picking up on a structural difference or a regime shift.

My questions are:

- Is there some mistake in my thinking? Is it correct that there should be a PnL drift induced by the skew decay and that this is not necessarily small? Has anyone ever tried to simulate this for the S&P and made a similar observation? It is of course possible that I made a mistake.

- It is not intuitively clear to me, why this strategy should only work for short maturity options. Basically all that is done to motivate it is to take a vol model quadratic in log moneyness and plug it into a Taylor expansion for the total option PnL. Where does this break down for, say a 90 day option, and is there a way to get something similar here?

Edit: Some additional observations

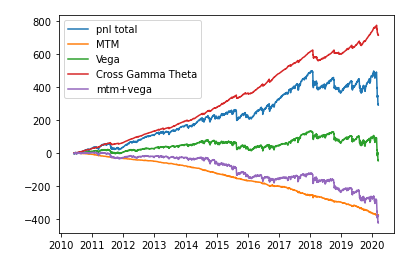

I am adding a plot with a decomposition for the PnL of the 35day 95/105 gamma neutral risk reversal for the S&P. Unfortunately I only have data until March 13 2020, so I am missing the interesting moves after this date. "PnL Total" is the PnL is the PnL of the position. "MTM" is the PnL from remarking the skew parameter and the quadratic ("vol of vol") parameter. "Vega" is the PnL from ATM moves and "Cross Gamma Theta" the PnL from dSdATM minus the theta. As can be seen from the plot, MTM brings a steady decay, as I suggested in my question. I would call this decay quite significant, as it basically eats up the PnL from Cross Gamma Theta since 2018.

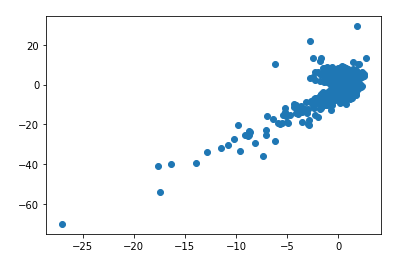

The following scatter plot show Cross Gamma Theta PnL on the x-axis vs the Vega hedged PnL of the risk reversal on y-axis. The regression beta (with 0 intercept) is 1.05 and R^2 is 76%.

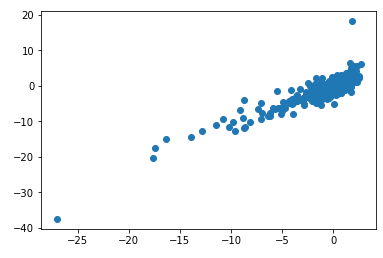

Now I am showing Cross Gamma Theta PnL on x-axis vs total PnL on y-axis. Regression beta is 2.38 and R^2 57%