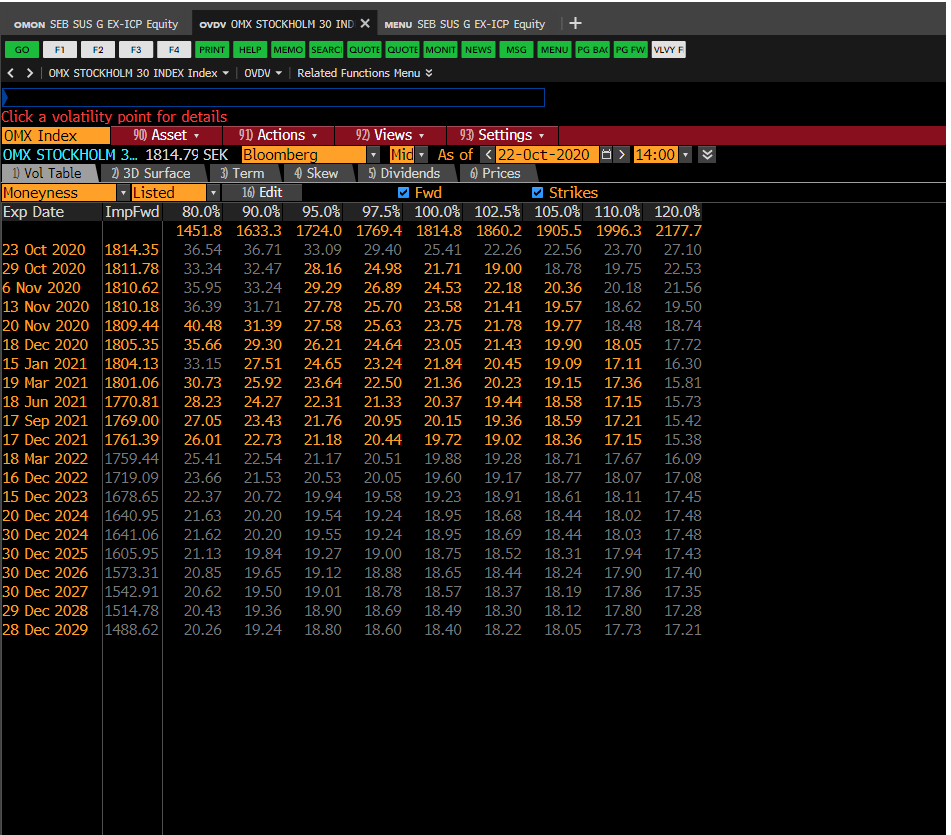

Should be a simple matter, but perhaps I'm misunderstanding something fundamentally. Look first at the below image of the BVOL surface from Bloomberg, to my understanding from looking at the white paper for the surface construction this surface is based on the implied forward of the underlying, which I have taken to mean that the moneyness quoted on the image (95%, 97.5%, 100%, 102.5%...) is the forward moneyness of the option. So what I'm expecting then is that an option with strike = implied forward for a given maturity has the implied volatility of the ATM node, e.g. a Jan 15 2021 option in the picture has an ATM volatility if it's strike is 1804.13 (and not 1814.79 which is the spot price). Playing around in the option valuation tool however I don't see this effect, it then seems that the option that has strike=spot=1814.79 has an implied volatility given by the ATM node at this maturity (that is 21.84%). Am I misunderstanding what it means for a surface to be defined by implied forward moneyness?