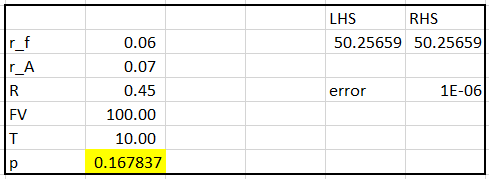

I have the following details: A 10-year U.S.Treasury strip has a yield of 6% and a 10-year zero issued by XYZ Inc, rated A by S&P and Moody's, has 7% (semi-annual compounding). Assuming a recovery rate of 45% What is the cumulative probability of XYZ Inc, defaulting during next 10 years?

How do I calculate the cumulative probability?